Rajasthan Board RBSE Class 12 Economics Chapter 1 Introduction to Economics

RBSE Class 12 Economics Chapter 1 Practice Questions

RBSE Class 12 Economics Chapter 1 Multiple Choice Questions

Question 1.

Who gave the wealth-oriented definition of Economics?

(a) Adam Smith

(b) Alfred Marshall

(c) Paul. A. Samuelson

(d) Koutsoyiannis

Answer:

(a)

Question 2.

The term ‘Varta’ has been used for:

(a) agricultural activity

(b) animal husbandry

(c) commerce

(d) All of these

Answer:

(d)

Question 3.

Micro economics is related with:

(a) prices of factors of production

(b) prices of services

(c) prices of goods

(d) All of these

Answer:

(d)

Question 4.

Macro, economics is related with:

(a) national income, economic growth and development

(b) general price level and level of employment

(c) levels of total savings and total investment

(d) All of these

Answer:

(d)

Question 5.

Which of the following is not a major economic problem?

(a) What to produce

(c) For whom to produce

(b) How to produce

(d) How to become poor

Answer:

(d)

RBSE Class 12 Economics Chapter 1 Very Short Answer Type Questions

Question 1.

To what is economics related ?

Answer:

Economics is related to the study of the economic aspect of the behaviour of economics of an individual or countries.

Question 2.

What is Micro Economics?

Answer:

Micro economics, may be defined as that branch of knowledge which studies the economic behaviour of the individual unit, which may be a person, a particular household or a particular firm.

Question 3.

What is Macro Economics?

Answer:

Macro economics is the branch of knowledge that studies the behaviour and performance of an economy as a whole.

Question 4.

Into how many sectors has economy been classified?

Answer:

Economy has been classified into three sectors:

- Primary sector (Agriculture and animal husbandry)

- Secondary sector (Production and manufacturing)

- Tertiary sector (Service sector).

Question 5.

On what basis is the decision taken in a capitalist economy?

Answer:

Decision of a capitalist economy is taken on the basis of cost, profit and minimum investment.

Question 6.

On what basis is the decision taken in socialist economy?

Answer:

In socialist economy, a decision is taken on the basis of socio-economic welfare.

RBSE Class 12 Economics Chapter 1 Short Answer Type Questions

Question 1.

What are the main areas of study of Micro Economics?

Answer:

Under micro-economics, the behaviour of economic units, i.e. individual, industries, wages, firms is studied in context of goods and services. Its main tools are demand and supply. It includes consumption, production, exhcnage, distribution, economic welfare, etc.

Question 2.

What are the main areas of study of Macro Economics?

Answer:

Under macro-economics, activities related to the entire economy are studied, i.e. total income-expenditure, total savings and investment, etc.

Question 3.

Mention the types of micro economics in a nutshell.

Answer:

Assuming the cost of a commodity to be variable and all other factors to be constant, the study of individual unit is called micro-economic study. But when all the factors are variable, such study is called total micro-economic study. When micro-economic study is done assuming price, etc., variables to be stable, it, is called micro-economic static study. Similarly, when two stable conditions are compared, it is called micro-economic comparative study, and study done by assuming economic variables to be in a continuously dynamic state, is called dynamic study.

Question 4.

What is production possibility curve?

Answer:

A production possibility curve is a curve which shows the various alternative production possibilities which can be employed with the given resources and techniques of production. It is also called Product Transformation Curve.

Question 5.

What is opportunity cost?

Answer:

When producing some additional quantity of a product, some quantity of another product has to be sacrified. This is called the opportunity cost of producing one additional unit of the product.

Question 6.

Briefly describe the inductive and deductive methods of economics.

Answer:

Deductive Method : This method deduces conclusions from fundamental assumptions or axioms established by other methods. It proceeds from reasoning to a study of facts and verifications of conclusions arrived at. The process of logic is from general to particular.

Inductive Method : The inductive method derives economic theories on the basis of observations and experiment. In this method, detailed data is collected with regard to a certain economic phenomenon.

RBSE Class 12 Economics Chapter 1 Essay Type Questions

Question 1.

Explain the relationship between scarcity and choice in detail.

Answer:

The element which gives rise to economic problem is that resources are scarce in relation to wants. If the resources, like wants, were unlimited, no economic problem would have arisen because in that case all wants would have been satisfied and there would have been no problem of choosing between all wants and allocating the scarce resources between them.

Because the resources are scarce, all wants cannot be satisfied. Therefore, human beings have to decide that for the satisfaction of which wants the resources should be used and which wants should be left unfulfilled. It should be noted that means or resources here refer to natural productive resources, man-made capital goods, consumer goods, money and time available with man, etc. If the means or resources were unlimited, then we would have obtained goods in the desired quantities because in that state of affairs goods would have been free goods. But in actual life, we cannot obtain goods freely or without price. We have to pay a price for them and make efforts to obtain them.

Resources or means have various alternative uses. In other words, the resources can be put to various uses. For instance, coal can be used as a fuel for the production of industrial goods, it can be used for running trains, it can be used for domestic cooking purposes and for so m.any other purposes. Likewise, monetary resources can be utilized for the production of essential consumer goods, for the production of capital goods and so many other goods. It has to be decided how the resources have to be allocated among different uses. The man or society has, therefore, to choose the uses for which resources have to be employed. If the resources had a single use only, the question of choice would not have arisen at all. In the case of single use of resources, they would have been employed for the uses for which they are meant. It is because of the various alternatives uses of the scarce resources that we have to decide about the best allocation of resources.

Thus, economic problem is the problem of scarcity and economics is the logic of choice. It is a challenge to scarcity. It tells us how man can use the best choice tackling the problem of scarcity of resources.

Question 2.

Describe the causes of the origin of the economy by mentioning the central problems of an economy.

Answer:

Human wants are unlimited and productive resources such as land and other natural resources, raw material, capital equipments etc. with which goods and services are produced to satisfy those wants, are scarce. The problem of scarcity of resources is felt not only by individuals but also by the society as a whole. This gives rise to the problem of how to use scarce resources to attain maximum satisfaction. This is generally called ‘the Economic Problem’. Every economic system, be it capitalist, socialist or mixed, has to deal with this central problem of scarcity of resources relative to wants for them. The central economic problem is further divided into four basic economic problems. These are:

(i) What to produce?

(ii) How to produce?

(iii) For whom to produce?

(iv) What provisions (if any) are to be made for economic growth?

(i) What to produce : Every society has to decide which goods are to be produced and in what quantities. Whether more guns should be produced or more butter should be produced; or whether more capital goods like machines, equipments, dams etc., will be produced or more consumer goods such as bread will be produced. Not only the society has to decide about what goods are to be produced, but it has also to decide in what quantities these goods would be produced. In a nutshell, a society must decide how much wheat, how many hospitals, how many schools, how many machines, how many metres of cloth, etc. have to be produced.

(ii) How to produce : There are various alternative techniques of producing a commodity. For example, cotton cloth can be produced with either handlooms or power looms or automatic looms. Production with fyandlooms involves use of more labour and production while automatic loom involves use of more machines and capital. A society has to decide whether it will produce cotton cloth using labour-intensive techniques or capital-intensive techniques. Likewise, for all goods and services, it has to decide whether to use labour intensive techniques or capital-intensive techniques. Obviously, the choice would depend on the availability of different factors of production (i.e., labour and capital) and their relative prices. It is in the society’s interest to use those techniques of production that make best use of the available resources.

(iii) For whom to produce : Another important decision which a society has to take is for whom to produce. The society cannot satisfy all the wants of all the people. Therefore, it has to decide who should get how much of the total output of goods and services. In other words, it has to decide about the share of different people in the national cake of goods and services.

(iv) What provision should be made for economic growth : A society would not like to use all its scarce resources for current consumption only. This is because if it uses all the resources for current consumption and no provision is made for future production, the society of the people would remain stagnant, and in the future, the level of living may decline. Therefore, a society has to decide how much savings and investment (i.e. how much sacrifice of current consumption) should be made for future progress.

Question 3.

Explain the main economic problems with the help of the concept of production possibility curve and opportunity cost.

Answer:

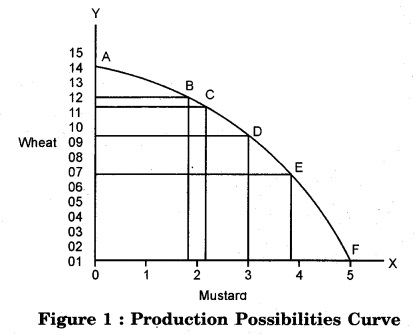

The central problems of economy can be very well explained with the help of Production Possibility Curve (PPC). The PPC is an analytical tool which is used to illustrate the problem of choice. So first, we will explain the concept of PPC.

Production Possibility Curve (PPC) : A production possibility curve is a curve which shows the various alternative production possibilities which can be produced with given resources and techniques of production. We know that there is a maximum limit which can be produced with given resources and techniques of production. In this situation, if we want to increase the production of a particular commodity, then we will have to reduce the production of some other commodity. This is why, production possibility curve is also known as Transformation Curve.

In Order to Understand PPC, Let Us Assume That There are Two Types of Goods – Wheat and Mustard which are to be produced. We also assume that

- there is a given amount of productive resources and they remain fixed

- resources are neither unemployed nor underemployed and

- technology does not change. Now consider the following table:

Table 1 : Alternative Production Possibilities

|

Production |

Mustard (in thousand quantals) |

Wheat (in thousand quintals) |

Marginal Opportunity Cost |

| A | 0 | 30 | – |

| B | 1 | 28 | 2 |

| C | 2 | 24 | 4 |

| D | 3 | 18 | 6 |

| E | 4 | 10 | 8 |

| F | 5 | 0 | 10 |

The above table shows various production possibilities between wheat and mustard. If all the given resources are employed for the production of wheat, 30 thousand quintals of wheat are produced. On the other hand, if all the resources are employed for the production of mustard, 5 thousand quintals of mustard are made. But these two are extreme production possibilities such as B, C, D and E. With production possibility B, the economy can produce with given resources one thousand quintals of mustard and 28 thousand quintals of wheat and with production possibility C, it can produce 2 thousand quintals of mustard and 24 thousand quintals of wheat. Thus, as the economy is moving from one possibility to another, it takes away some resources from wheat and put them in the production of mustard. Since resources are limited and we have assumed that they are fully employed, the economy has to give up something of one good to obtain some more of the other.

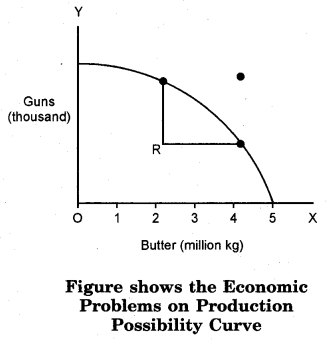

The production possibilities shown above can be illustrated diagrammatically also as is shown in the figure 1.

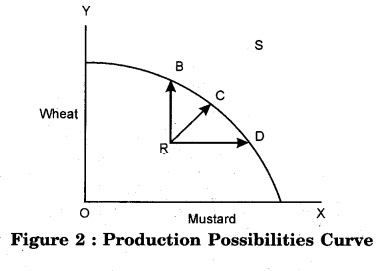

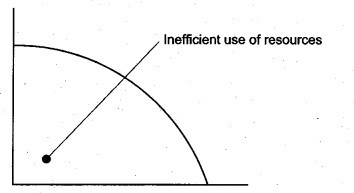

The curve AF is called Production Possibilities Curve (PPC) or Production Possibilities Frontier (PPF). This curve shows the various combinations of two goods which the economy can produce with a given amount of resources. Since the given resources are fully employed and utilized, the combination of two goods produce can lie anywhere on the production possibilities curve AF but not inside or outside it. For example, the combined output of two goods can neither lie at R nor at S (Figure 2). This is because at point R the economy would not be utilizing its resources fully, and at point S, the economy would not have capability to produce with the given technology.

In the context of PPC, since, there are only two goods, therefore opportunity cost of producing one good is in terms of sacrifice made of the other good. In table 1, we have found opportunity cost of producing additional units of mustard in terms of wheat. Thus, as the economy moves from possibility A to possibility B, it has to give up one thousand quintals of wheat in order to have one thousand quintals of mustard. Thus, first thousand quintals of mustard have the opportunity cost of one thousand quintal wheat to the economy. But as we step up, and move further from B to C, extra two thousand quintals of wheat have to be foregone for producing extra one thousand quintals of mustard. In other words, opportunity cost goes on increasing as we have more of mustard and less of wheat. It is this principle of increasing opportunity cost that makes the PPG concave to the origin.

If opportunity cost constant, PPC would be a straight line. But generally, we get increasing opportunity costs. This is because a given resource is suitable more for the production of wheat than mustard. As we increase the production of mustard, resources which are less productive in the production of mustard would have to be pushed in it. Thus, more units of that resource would be required to produce mustard. In other words, greater sacrifice would have to be made in terms of production of wheat for every extra production of mustard. This laws holds good if we move from A to F or from F to A on the PPC.

Question 4.

Describe the key assumptions of economic analysis.

Answer:

A systematic approach to determining the optimum use of scarce resources, which includes comparison of two or more options in achieving a specific purpose, lie under the assumptions and constraints. Economic analysis takes into consideration the fundamental costs of resources in account and attempts to measure personal and social costs and the benefit of the community or the economy in monetary terms. The key assumptions of economics analysis are given below:

(i) On the Basis of Dependence

(a) Partial Analysis : When economic analysis is done while considering a single factor, it is called Partial Analysis. For example, the study of demand, in relation to commodity price.

(b) General Analysis : When economic analysis is done considering multiple factors, it is called General Analysis. For example, the demand of commodity in relation to its prices as well as other factors.

(ii) On the Basis of Time Element

(a) Static Analysis : When economic analysis is done on the basis of particular point of time, it is called Static Analysis.

(b) Comparative Analysis : When economic analysis is done on the basis of two points of time, it is called Comparative Analysis.

(c) Dynamic Analysis : When economic analysis is done on the basis of changes in equilibrium of services, it is called Dynamic Analysis.

(iii) On the Basis of Tools and Direction

(a) Deductive Method : When economic analysis is done on the basis of general truth or the economic analysis of a specific individual unit.

(b) Inductive Method: When economic analysis is done on the basis of reasoning (logic). We proceed in this method from reasoning to a study of facts and verifications of conclusions arrived at. The process of logic is from general to particular.

Question 5.

Describe in detail the differences between micro and macro economics.

Answer:

The main differences between micro and macro-economics are as given below :

| Basis of Difference | Micro-economics | Macro-economics |

| 1. Sphere | Micro-economics studies individual units, i.e. person, firm, family, industry, etc. and their problems. | Macro-economics studies total consumption, total investment total national income, etc. on total economy level. |

| 2. Assumption | In micro-economic studies, all macro-variables are taken to be constant. | In macro-economic studies, all micro-variables are taken to be constant. |

| 3. Objective | Its main objective is the best (optimum) distribution of resources. | Its main objective is the complete utilisation and development of resources. |

| 4. Main problem | Its main problem is price determination. | Its main problem is determination of income and employment. |

| 5. Tool | Its tool is demand and supply. | Its main tool is the total demand and total supply of the economy. |

| 6. Change | Micro-changes can occur in constancy of macro-factors. | The stability of macro-factors is not affected by changes in structure of micro-factors. |

| 7. Contradiction | Savings are beneficial for micro-levels. | Savings are not beneficial for macro-levels. |

| 8. Relationship | Micro-economics is related to an individual firm or industry and its production and determination of price. | Macro-economics is related to the total production and general price level determination in total economy. |

Question 6.

Discuss in detail that economics is both a science and an art.

Answer:

Often a question arises : Whether economics is a science or an art or both. A subject is considered science if it is a systematized body of knowledge which studies the relationship between cause and effect, it is capable of measurement, it has its own methodological apparatus and it has the ability to forecast. If we analyse Economics, we find that it has all the features of science. Like science, it studies cause and effect relationship between economic phenomena.

To understand, let us take the law of demand. It explains the cause and effect relationship between price and demand for a commodity. It says, given other things to be constant, as price rises, the demand decreases. Similarly, like science, it is capable of being measured, the measurement is in terms of money. It has its own methodology of study (induction and deduction) and it forecasts the future market conditions with the help of various statistical and non-statistical tools.

Economics is an art. Art is nothing but practice of knowledge. Where science teaches us to know, art teaches us to do. Unlike science which is theoretical, art is practical. If we analyse. Economics, we find that it has the features of an art also. Its various branches — consumption, production and public finance, etc. provide practical solutions to various economic problems. It helps in solving various economic problems which we fiice in our day-to-day life.

Thus, Economics is both a science and an art. It is science in its methodology and art in its application. Study of the problem of unemployment is science but framing suitable policies for reducing the extent of unemployment is an art.

RBSE Class 12 Economics Chapter 1 Other Important Questions – Answers

RBSE Class 12 Economics Chapter 1 Multiple-Choice Questions

Question 1.

The Father of Economics in the world is :

(a) Adam Smith

(b) Alfred Marshall

(c) Lord Lionel Robbins

(d) Prof. J. K. Mehta

Answer:

(a)

Question 2.

Economist Alfred Marshall has described economics as the :

(a) study of wealth

(b) study of economic welfare

(c) study of unlimited wants and limited resources

(d) none of these

Answer:

(b)

Question 3.

He used the term ‘micro’ for the first time :

(a) Marshall

(b) Bolding

(c) Keynes

(d) Regner Fristch

Answer:

(d)

Question 4.

Regner Fristch first used the terms micro-economics and macro-economics:

(a) in 1776

(b) in 1933

(c) in 1977

(d) in 1934

Answer:

(b)

Question 5.

Micro-economics studies :

(a) a consumer

(b) a producer

(c) a firm

(d) all of the above

Answer:

(d)

Question 6.

This is not related to macro-economic analysis :

(a) national income

(b) international trade

(c) fiscal policy

(d) Price theory

Answer:

(d)

Question 7.

The author of the book ‘The General Theory’ is :

(a) John Maynard Keynes

(b) Adam Smith

(c) Marshall

(d) Regner Fristch

Answer:

(a)

Question 8.

Economics is a science because it :

(a) Establishes a relationship between cause and effect

(b) Propounds universal principles

(c) Uses scientific methods

(d) all of these

Answer:

(d)

Question 9.

The problem of choice arises :

(a) because of limited resources

(b) because of unlimited wants

(c) because of both (a) and (b)

(d) none of these

Answer:

(c)

Question 10.

This is a feature of mixed economy system :

(a) Private ownership on resources

(b) Ownership of society on resources

(c) both private and government ownership on resources

(d) none of these

Answer:

(c)

RBSE Class 12 Economics Chapter 1 Very Short Answer Type Questions

Question 1.

Give the ‘wealth’ definition of economics.

Answer:

According to Adam Smith, “Economics is concerned with “an Inquiry into the nature and causes of wealth of nations” and it is related to the laws of production, exchange, distribution and consumption of wealth”.

Question 2.

What is the ‘welfare’ definition of economics? .

Answer:

According to Prof. A.C. Pigou, “The range of our enquiry becomes restricted to that part of social welfare that can be brought directly or indirectly into relation with measuring-rod of money.”

Question 3.

Give Robbins’ (scarcity) definition of economics.

Answer:

According to Robbins, “Economics is the science which studies human behaviour as a relationship between ends and scarce means which have alternative uses.”

Question 4.

What is the ‘growth-oriented’ definition of economics?

Answer:

According to Samuelson, “Economics is the study of how people and society end up choosing with or without the use of money to employ scarce productive resources that could have alternative uses, it produces various commodities and distributes them for consumption now or in the future, among various persons and groups in society.”

Question 5.

Define human wants.

Answer:

Human ‘want’ is an effective desire for a particular thing, which can be satisfied by msiking an effort to acquire it.

Question 6.

What is consumption?

Answer:

The act of using goods and services to satisfy human wants is called Consumption. According to Meyers, “Consumption is the direct use of goods and services in satisfying the human wants.”

Question 7.

Define utility.

Answer:

Utility refers to want-satisfying power of a commodity. According to Prof. Hibdon, “Utility is the ability of goods to satisfy a want.”

Question 8.

Define scarcity.

Answer:

Scarcity means that we do not and cannot have enough to satisfy our every desire. It means that goods are scarce relative to their wants. Scarcity is a key factor of economic life.

Question 9.

What is the problem of choice?

Answer:

Since resources are limited, society has to choose between the alternative uses of the available resources. This is known as the Problem of Choice.

Question 10.

Write one importance of micro economics.

Answer:

Helpful in analysis of the individual unit problem.

Question 11.

What is the other name of micro-economies?

Answer:

Theory of cost.

Question 12.

What was the basis of early man’s livelihood?

Answet:

Hunting.

Question 13.

What is the definition of macro-economics according to Gardner Ackley?

Answer:

According to Gardner Ackley, “Macro-economics concerns itself with such variables as the aggregate volume of the output of an economy, within the extent to which its resources are employed, with the size of national income and with the general price level.”

Question 14

Who defined economics as a study of wealth?

Answer:

Adam Smith.

Question 15.

Can you imagine a situation of scarcity without the problem of choice?

Answer:

No, I cannot imagine a situation of scarcity without the problem of choice because scarcity and choice are inseparable at all levels of decision-making.

Question 16.

What kind of units are studied under the subject matter of micro economics?

Answer:

Individual unit.

Question 17.

What is meant by production?

Answer:

Production is that activity which is based on or related to the use of scarce resources for the satisfaction of human wants.

Question 18.

What is product pricing?

Answer:

Product pricing involves the to determination of the price of the product under different conditions of the market, viz. perfect competition, monopoly and imperfect competition.

Question 19.

What is meant by market?

Answer:

Market refers to a mechanism or an arrangement that facilitates contact between the buyers and sellers for the sale and purchase of goods and services.

Question 20.

Define investment.

Answer:

Investment is that economic activity which is concerned with the purchase of capital goods for further production. It enhances production capacity of the producers.

Question 21.

What is national income?

Answer:

National income is defined as the value of all final goods and services produced by the residents of a country in a year.

Question 22.

What is economic welfare?

Answer:

Pigou defines economic welfare as that part of social welfare that can be directly or indirectly measured in money.

Question 23.

Define social welfare.

Answer:

Social welfare is defined as the sum total of the happiness of all the individuals in the society.

Question 24.

What does the problem ‘for whom to produce’ refer to?

Answer:

For whom to produce means how is the total output of goods and services produced in the economy to be divided among its members. Who shall get the goods and services produced in the economy?

Question 25.

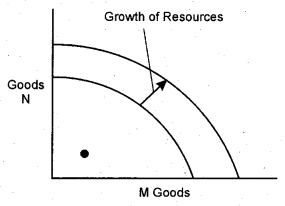

What does a rightward shift of production possibility curve indicate?

Answer:

A rightward shift of production possibility curve indicates that resources have increased.

Question 26.

Why does an economic problem arise?

Answer:

Economic problem arises because of resource allocation.

Question 27.

What is central problem of economy?

Answer:

Central problem of economy means the problems that are common and fundamental to all economies. These problems are various manifestations of the basic problem of scarcity of resources.

Question 28.

What are the properties of PPC?

Answer:

Two basic properties of PPC are given below:

- Production possibility curve slopes downward.

- Production possibility curve is concave to the point of origin.

Question 29.

What does a point within the production possibility curve show?

Answer:

A point within the production possibility curve shows the under-utilization of resources.

Question 30.

What is the problem of economic efficiency?

Answer:

This is the problem of putting resources to their best possible use.

Question 31.

Who is the author of the book, ‘The General Theory of Employment Interest and Money’?

Answer:

John Maynard Keynes.

Question 32.

Define Partial analysis on the basis of dependence.

Answer:

When economic analysis is done while considering a single factor, it is called Partial Analysis.

Question 33.

Define General analysis on the basis of dependence.

Answer:

If the demand of a commodity in relation to its prices as well as other factors is studied, this analysis is called General Analysis.

Question 34.

Define static analysis on the basis of time element.

Answer:

When economic analysis is done on the basis of particular point of time, it is called Static Analysis.

Question 35.

Define comparative analysis on the basis of time element.

Answer:

If the analysis is done on the basis of two points of time, it is called Comparative Analysis.

Question 36.

Define dynamic analysis on the basis of time element.

Answer:

If the services change in equilibrium with time, it is called Dynamic Analysis.

Question 37.

Define priori method on the basis of tool and direction.

Answer:

When generalization is made on the basis of reasoning (logic), it is called Priori Method.

Question 38.

Define inductive method.

Answer:

It is the method which drives economic theories on the basis of observation and experiment.

Question 39.

What is marginal opportunity cost?

Answer:

Marginal opportunity cost refers to the amount of a good sacrificed in order to- produce a single additional unit of another good. v

Question 40.

What is economic development?

Answer:

Economic development has been defined as a sustained increase in real per capita income.

RBSE Class 12 Economics Chapter 1 Short Answer Type Questions (SA-I)

Question 1.

How is ‘choice’ a core parameter in the study of economics?

Answer:

Choice is the consequence of scarcity. Choice emerges when limited resources are to be used for the satisfaction of unlimited wants. A rupee cannot buy ten things when the price of each thing is ₹ 1. You have to choose the thing you would prefer to have; you have to forego nine things in favour of the one thing you choose to have. Choosing one alternative and not choosing others is a problem of choice. It is also called Economic Problem; it stems out of scarcity.

Question 2.

State the theories that we study in micro economics.

Answer:

- Theory of demand and consumer behaviour.

- Theory of supply and producer behaviour.

- Production theories explaining how production responds to different combinations of inputs.

- Theory of price determination, explaining how prices of goods and services are determined in different markets.

Question 3.

What is meant by economising of resources?

Answer:

Economising of resources means that the available resources should be allocated among different uses in such a way that the resources are put to their best possible use.

Question 4.

Write two features each of positive economics and normative economics.

Answer:

Positive Economics

- Positive economics is that science in which analysis is confined to cause and effect relationship.

- Positive economics is concerned with the facts about the economy.

Normative Economics

- Economics as a normative science is concerned with what ‘ought to be’.

- Normative economics deals primarily with economic goals of a society and the policies adopted to achieve certain goals.

Question 5.

Give the meaning of economic problem.

Answer:

Economic problems arise from the scarcity of resources relative to human wants. Since the society cannot satisfy all its wants due to limited availability of goods and services, it must make a choice as to which wants are to be satisfied and which wants need to be left unfulfilled for the time being. Since resources are limited, society has to choose between the alternative uses of the available resources. This is known as the Problem of Choice or economic problem.

Question 6.

Give any two assumptions of production possibility curve.

Answer:

Two assumptions of production possibility curve are:

- Resources are fully and efficiently utilized.

- Technique of production remains constant.

Question 7.

Point out two characteristics of the production possibility curve.

Answer:

Two characteristics of the production possibility curve are :

- The production possibility curve slopes downwards to the right.

- It is concave to the origin.

Question 8.

What are the three central problems of an economy? Why do they arise?

Answer:

Human wants are unlimited and productive resources such as land and other natural resources, raw materials, capital equipments, etc. with which goods and Services are produced to satisfy those wants, are scarce. The problem of scarcity of resources is felt not only by individuals but also by the society as a whole. This gives rise to the problem of how to use scarce resources to attain maximum satisfaction. This is generally called ‘the Economic Problem’. Every economic system, be it capitalist, socialist or mixed, Ms to deal with this central problem; of scarcity of resources relative to wants for them.

Question 9.

Explain the problem ‘what to produce’ with the help of an example. Does it arise in every economy? Explain.

Answer:

Every society has to decide which goods are to produced and in what quantities. Whether more guns should be produced or more butter should be produced; or whether more capital goods like machines, equipments, dams, etc. will be produced or more consumer goods such as bread will be produced. The society not only has to decide about what goods are to be produced, but it has also to decide in what quantities these goods would be produced. In a nutshell, a society must decide how much wheat, how many hospitals, how many schools, how many machines, how many meters of cloth, etc. have to be produced.

Yes, this problem arises in every economy because this problem is not only related to the individual, but it is also related to large society, large industries and government.

Question 10.

Explain the problem of ‘how to produce1. Why does this problem arise?

Answer:

There are various alternative techniques of producing a commodity. For example, cotton cloth can be produced with either handlooms or power looms or automatic looms. Production with handlooms involves use of more labour and production while automatic loom involves use of more machines and capital. A society has to decide whether it will produce cotton cloth using labour-intensive techniques or capital-intensive techniques. Likewise, for all goods and services, it has to decide whether to use labour-intensive techniques or capital intensive techniques. Obviously, the choice would depend on the availability of different factors of production (i.e., labour and capital) and their relative prices. It is in the society’s interest to use those techniques of production that make best use of the available resources.

Question 11.

Explain the problem ‘for whom to produce’.

Answer:

Another important decision which a society has to take is for whom to produce. The society cannot satisfy all wants of all the people. Therefore, it has to decide who should get how much of the total output of goods and services. In other words, it has to decide about the shares of different people in the national cake of goods and services.

Question 12.

Distinguish between total utility and marginal utility.

Answer:

Total utility refers to the entire amount of satisfaction obtained from consuming a given quantity of a commodity. According to Lipsey, “Total utility refers to the total satisfaction from the amount of the commodity consumed.”

Marginal utility is the additional utility which results from a unit increase in consumption. According to Prof. Boulding, “The marginal utility is the utility which results from a unit increase in consumption.”

Question 13.

State the main features of wealth definition of economics.

Answer:

The main features of wealth definition of economics are:

- Study of Wealth : Economics is the study of wealth only. The main object of economics is to examine how people earn wealth and spend wealth.

- Causes of Wealth : Economics seek to examine causes which lead to increase in wealth. Wealth can be increased by its production and accumulation.

- Economic Man : The wealth definition of economics takes the notion of economic man who is aware of his self-interest. The economic man tries to achieve his self-interest by increasing his material gains through acquisition of wealth.

Question 14.

Is economics an art or a science or both?

Answer:

Economics is both a science and an art. As a science, economics is a systematic body of knowledge which makes generalization and theories by adopting scientific approach. As an art, it puts this knowledge into practice. It uses economic theories and laws in formulating various economic policies. Thus, economics is ‘science’ in methodology and ‘art’ in its application. Corsa observed that science requires arts, and arts require science, each being complementary to the other.

Question 15.

In what sense is economics a normative science?

Answer:

As a normative Science, economics involves value judgement. It is prescriptive in nature and describes ‘what should be the things’. For example, the question like what should be the level of national income, what should be the wage rate, how can the fruits of national product be distributed among people, all fall within the scope of normative science. Thus, normative economics is concerned with welfare propositions. Some economists are of the view that value judgements by different individuals will be different, and thus for deriving laws or theories, it should not be used.

Question 16.

Discuss the concept of opportunity cost with an example.

Answer:

Stocks of resources available to a community are given. When the community decides to channel its resources in the production of certain commodities, then they have to abandon some other products which the community could have produced with these resources. From the perspective of a society using a resource for any purpose, it means that we want to sacrifice that good. Those resources that encourage their current use, are called the Cost of Opportunity.

In essence, the cost of production of an object is that quantity of other items which we have to sacrifice.

Example : A carpenter, in one day, can make either one table or 2 chairs. The opportunity cost of 1 table = 2 chairs which can be made instead of a table.

Question 17.

What does slope of PPC show?

Answer:

Production possibility curve is concave to the origin. Its increasing slope shows that more and more of commodity Y (on the Y-axis) is to be sacrificed for every additional unit of commodity X, or in other words, the cost of producing additional X tends to increase in terms of the loss of Y. This is in accordance with the principle of diminishing returns or increasing cost of production.

Question 18.

Differentiate between capitalist economy and socialist economy.

Answer:

Difference between capitalist and socialist economy :

Capitalist Economy

(i) It has right of private property, means that productive factors such as land, factories, machinery, mines, etc. are under private ownership. The owners of these factors are free to use them in the manner in which’ they like. The government may, however, put some restrictions for the benefit of the society in general.

(ii) It comprises freedom of enterprise, means that everybody engages in any economic activity which they like.

(iii) It allows freedom of choice to the consumer, means people in a capitalist economy are free to spend their income as they like. This is known as Consumer Sovereignty.

(iv) It is a profit-motive economy which forces or induces people to work and produce.

(v) In this economy, competition prevails among sellers to sell their goods and among buyers to obtain goods to satisfy their wants. Advertisement, price-cutting, discounts, etc. are very common methods of competition in a capitalist economy.

Socialist Economy

(i) It possesses collective ownership of means of production, except small farms, workshops and trading-firms which may remain in private hands. As a result of social ownership, profit-motive and self-interest are not the driving force of economic activity as it is in the case of market economy.

(ii) It has central authority to establish and accomplish socio-economic goals; that is why it is called Centrally Planned Economy. Major economic decisions, such as what to produce, when and how much to produce, etc. are taken by the central authority.

(iii) In this economy, freedom from hunger is guaranteed but consumers’ sovereignty gets restricted by selective production of goods. The range of choice is limited by planned production. However, within that range, an individual is free to choose what he likes most.

(iv) A relative equality of income is an important feature of this economy. Among other things, differences are narrowed down by lack of opportunities to accumulate private capital. Educational and other facilities are enjoyed more or less equally; thus the basic causes of inequalities are removed.

(v) Pricing mechanism exists in a socialist economy but it has only a secondary role, e.g., to secure disposal of accumulated stocks. Since allocation of productive resources is done according to a pre-determined plan, the pricing mechanism loses its predominant role in economic decisions.

Question 19.

What is meant by mixed economy?

Answer:

In a mixed economy, the aim is to develop a system which tries to include the best features of both the controlled economy and the market economy while excluding the demerits of both. It appreciates the advantages of private enterprise and private property with their emphasis on self-interest and profit motive. Rapid economic development of England, the USA, etc. was due to private enterprise. At the same time, it says that private property, profit motive and self-interest of the market economy may not promote the interests of the community as a whole, and as such, the government should remove these defects of private enterprise. For this purpose, the government itself must manage important and selected industries and eliminate the free play of the profit motive and self-interest. Private enterprise, which has its own significance, is also allowed to play a positive role in a mixed economy.

Question 20.

What are the features of mixed economy?

Answer:

The first important feature of a mixed economy is the co-existence of both private and public enterprise. In fact, in a mixed economy, there are three sectors of industries:

(i) Private Sector : Production and distribution is managed and controlled by private individuals and groups. Industries in this sector are based on self-interest and profit- motive. The system of private property exists and personal initiative is given full scope.

(ii) Public Sector : Industries in this sector are not primarily profit-oriented but are set up by the state for the welfare of the community.

(iii) Joint Sector : A sector in which both the government and the private enterprises have equal access, and join hands to produce a commodity, leading to the establishment of joint sector.

Secondly, a mixed economy is a planned economy, i.e., an economy in which the government has a clear and definite economic plan.

Thirdly, in a mixed economy, balanced regional development is expected.

Fourthly, in a mixed economy, a dual system of pricing exists.

RBSE Class 12 Economics Chapter 1 Short Answer Type Questions (SA-II)

Question 1.

What is economics?

Answer:

Economics is the study of how men and society choose, with or without the use of money, to employ scarce productive resources which could have alternative uses, to produce various commodities over time and distribute them for consumption now and in the future amongst various people and groups of society.

Question 2.

For which economic activity this given statement has been used?

“कृषि पालन पालय वाणिज्यम च वार्तः”

Answer:

For agricultural economic activities.

Question 3.

What are the economic definitions given by economists on different subject- matters?

Answer:

The main definitions given by economists are:

- Wealth centered

- Welfare centered

- Wantlessness centered

- Scarcity centered

- Growth centered.

Question 4.

What is the definition of economics as given by Prof. J.K. Mehta?

Answer:

Mehta has defined Economics as a science which studies human behaviour as a means to achieve the end of wantlessness.

Question 5.

What study is done in the theory of consumption under micro-economics?

Answer:

We study the diminishing marginal utility, equi-marginal utility, consumer optimization, savings of consumer, law of demand, elasticity of demand, etc. in theory of consumption.

Question 6.

Give some points on the importance of micro-economics.

Answer:

The importance of micro economics are:

- Helpful in analysis of the individual unit problem.

- Helpful in determining the value of goods and services.

Question 7.

Mention the names of Indian thinkers related to economics.

Answer:

The names of major Indian thinkers related to economics are: Swami Dayanand Saraswati, Dadabhai Naoroji, Mahadev Govind Ranade, Gopal Krishna Gokhale, Ramesh Chandra Dutt, M.N. Roy.

The later main thinkers related to economics are: Mahatma Gandhi, Jawaharlal Nehru, Ram Manohar Lohiya, Prof. J. K. Mehta, Pandit Deen Dayal Upadhyay and Amartya Sen.

Question 8.

How does A. Koutsoyannis define economics?

Answer:

According to A. Koutsoyannis, “Objective of economic theories is to build up a model of economic behaviour of an individual unit (may be one consumer, a producer or firm or government-agency) and its impact on one another, which constitute the economy of an area, a country or whole world.”

Question 9.

What is the subject matter of microeconomics?

Answer:

It is the study of all theories and principles which are based on individual unit. Following are included in the subject matter of micro-economics:

- Theory of consumption

- Theory of production

- Theory of price of commodity

- Theory of cost of resources.

Question 10.

Write down three utilities of micro-economics.

Answer:

Following are the three utilities of micro economics:

- It is helpful in taking decisions related to individual units.

- It is helpful in determining the value of goods and services.

- It is helpul in forecasting the market.

Question 11.

What is the general classification of economy?

Answer:

The economy is classified into:

- Primary sector (Agriculture and animal husbandry)

- Secondary sector (Production and manufacturing)

- Tertiary sector (Service sector).

Question 12.

Write down three utilities of macro-economics.

Answer:

Following are the three utilities of macro-economics:

- The function of the economy is better understood with the help of macro-economic analysis.

- Macro-economics plays an important role in economic planning of a country.

Question 13.

Micro and macro-economics are complementary to each other. Clarify it.

Answer:

Micro and macro-economics complement each other because its value depends on the demand of the whole economy at the time of purchase of raw materials or machines, etc. Apart from this, to influence the behaviour of different units, the general application of the economic knowledge of the principles is required to acquire the knowledge of its nature.

Question 14.

State two characteristics of micro-economics.

Answer:

- We study individual or specific units in micro-economics.

- We study small variables of economy in micro economics.

Question 15.

Write down four points related to the subject matter of macro economics.

Answer:

- Theory of income and employment

- Theory of normal price level

- Theory of business cycle

- Theory of money and banking.

Question 16.

What are the economic problems that arise due to limited resources?

Answer:

Following are the economic problems arising due to limited resources:

- Unlimited wants of different priorities.

- Limited resources, but having alternative uses.

- Co-ordination between wants and resources.

Question 17.

What are the characteristics of production possibility curve?

Answer:

- PPC is concave to origin (to the base point).

- PPC is made up of a combination of two objects, the combination of alternative possibilities of production.

- When the production possibility curve situation moves from one point to another, the combination of two objects changes.

Question 18.

Draw the diagram of production possibility curve.

Answer:

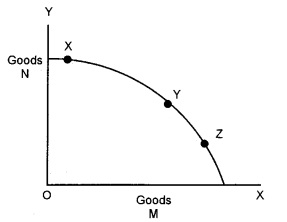

Question 19.

What do points X, Y and Z indicate on the production possibility curve?

Answer:

The points given on the production possibility curve indicate that the use of resources is being done efficiently.

Queston 20.

Make a production possibility curve showing the inefficient use of resources.

Answer:

Question 21.

Make a production possibility curve showing the growth of resources.

Answer:

Question 22.

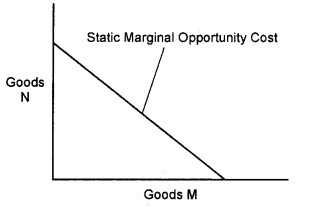

Make a production possibility curve which shows the static marginal opportunity cost.

Answer:

Question 23.

Write down two central problems of economy.

Answer:

- What to produce?

- How to produce?

Question 24.

How can one solve the problem of ‘what to produce’ in the capitalist economy?

Answer:

It is the second main problem of economy. It is related with the technical choice of goods and services. An economy has to choose whether labour-intensive technique or capital-intensive technique is appropriate.

RBSE Class 12 Economics Chapter 1 Long Answer Type Questions

Question 1.

Explain the subject matter of economics as clearly as you can.

Answer:

The subject matter of economics is presently divided into two major branches:

Micro-economics and macro-economics, these two terms have now become of general use in economics.

Micro-Economics : It studies the economic behaviour of individual economic units and individual economic variables. The unit of study in micro-economics is the part of the economy, such as individual households, firms and industries. Thus, the study of economic behaviour of the households, firms and industries forms the subject matter of micro economics. In other words, micro economics is a microscopic study of the economy. For example, microeconomics is concerned with how the individual consumer distributes his income among various products and services so as to maximize utility. Micro-economics also seeks to explain how the individual firms determine the sale price of the product, how much to produce, what amount of product will maximize its profit, how to minimize the cost of production.

Macro-Economics : Macro economics is the study of the economy as a whole. The unit of study in macro economics is the entire economy rather than a part of it, and it deals with the problems faced by the entire economy. Thus, macro economics deals with the functioning of the economy as a whole. For example, macro economics seeks to explain how the economy’s total output of goods and services and total employment of resources are determined and what explains the fluctuations in the level of output and employment. Macro economics explains why sometimes economy is operating at near-about full employment, and why, at other times, there is high degree of unemployment; why sometimes there is full utilization, of the economy’s productive capacity, and why, at other times, there is under-utilization of the economy’s productive capacity.

Question 2.

What is the ‘welfare’ definition of economics? Mention the features and criticism of this definition.

Answer:

“Economics is a study of the common activities of human life. It examines the part of that personal and social work that is best connected to the acquisition and with the physical needs of welfare. Thus, on one side, study of wealth and other important aspects, is a part of human study.”

The key features of the of welfare definition of economics are given below:

(i) Study of Mankind : Marshall laid primary emphasis on the study of mankind. There is no doubt he emphasizes both humankind and wealth in his definition. He has agreed with the classical economists that economics is concerned with money because money is essential for money. Money provides means for survival, comfort and happiness. But he believed that money is not everything, rather it is only a means for human welfare. Thus, it is the study of human being which is central to the study of economics.

(ii) Study of Simple Business of Life : Economics is a study of simple business of life. The general business of life is concerned about income-earning and income- expenditure activities of mankind. Economics studies how people take advantage of their livelihood resources and how they spend them for the satisfaction of their welfare.

(iii) Study of Material Welfare : Marshall emphasized on physical welfare as the primary concern of economics. According to him, economics is not related to total human welfare, but is related to physical welfare, that is, the part of human welfare that is related to money. Economics studies those activities which are closest to the “physical needs of receipt and welfare that they are connected to”.

(iv) Emphasis on the Things Needed for Welfare : Even the need for welfare substances is also emphasized. Obviously, physical things like food, clothing and shelter are very important economic objectives. The material needs are very basic needs that must be fulfilled before thinking about any other needs.

(v) Exclusion of Non-Economic Activities : Marshall has limited the scope of economics to those forces and activities which are eligible for measurement in terms of money. That is why the political, social, cultural and religious activities of humans are excluded from the scope of economics because they are not subject to be measured in terms of money.

The criticism of the definition of welfare is given below:

(i) Economics is Considered to be Just a Social Science : Marshall has been criticized for treating economics as a social science rather than a human science. As a Society member, he studies the work of people living in organized communities, while a human may be living in a community or be a member of an organized community, and he may also be living in isolation.

(ii) Unethical Classification of Activities: The criticism of Robbins is that the difference between economic and non-economic activities is unscientific, rational and misleading because all human activities have an economic aspect.

(iii) Only Materialistic Aspect: Robbins has criticized the definition of welfare saying that it includes only material things in its scope. It does not include non-material things like doctors, lawyers, teachers, etc. in its class. They do not have, any place ^ in services. However, these services meet our urgent needs and thus promote welfare.

(iv) Restricted Area of Economics : Robbins has also criticized the definition of welfare because it restricts the scope of study of economics. Economics studies many activities that minimize financial well-being, many things like alcohol, cigarette and gun do not promote economic welfare.

(v) The Ambiguous Concept of Material Welfare : The definition of welfare is also under criticism on the basis that physical well-being cannot be measured quantitatively. Welfare is a subjective thing. It is mental in nature, it is related to the mental make-up of a person. It varies according to time, place and person. In this way, welfare cannot be measured in objective terms.

Question 3.

“Scarcity is the root of the problem of choice which every economic system has to face.” Discuss the basic problem of an economic system illustrating your answer with the use of production possibility curve.

Answer:

Basic economic problems, i.e. shortage and selection problems, and some central problems can be illustrated with the help of production potential curve.

(i) Problems of Shortage : It is rooted in all those combinations of those objects which are beyond the likelihood of productivity, such as the combination given by point D in the figures given in combination. Production possibilities obtain points outside the range of combinations that cannot be obtained because adequate resources are not available to produce. This is the only point in or within the probability curve of productipn, which are attainable, i.e. combination, which can be produced with available resources.

(ii) Problem of Choice : This indicates the need to choose from the available points on the production potential curve, such as the combination between combination A and B.

(iii) What is to be Created : The problem of production of two goods from any point on the production possibility is the problem of what to produce. Different points on the curve represent different combinations of two objects. Thus, if the society chooses combination A, it shows that it has decided to produce more guns and less butter. On the other hand, if it chooses combination B, it shows that more butter will be produced. At what point should either product be produced, depends on the taste and preferences of the people in the economy.

(iv) Problems of Full and Efficient Use of Resources : If all resources are used fully and efficiently, then the production possibility curve will be operative at some points. But if the economy is producing any combination within the probability curve of its production, such as point C, it would mean that some of its resources remain unutilised and only some of its resources are used in production. Through efficient and full use of resources, the economy can move beyond C and go to any point on the production prospect curve. For example, by transferring B, forgoing one or more units of butter can produce more guns.

Question 4.

“Economics is both a positive and normative science.” Discuss.

Answer:

It is important to know the difference between positive economics and standard economics. Positive economics has been explaining what it is, that is, it describes the principles and laws for explaining the observed economic events, while standard economics is concerned with about what should be. Keynes distinguishes between two types of economics in the following way: “A positive science can be defined as the body of systematic knowledge, about what it is; an authentic science or a regulatory science, while normative science is a part of systemic knowledge related to the norms of what should be.”

Thus, in positive economics, we obtain proposals, principles and laws in pursuance of some rules of logic. These principles, law and propositions explain the relationship between cause and effect in economic forms. In positive micro economics, we are largely concerned with the determination of relative prices and allocation between different commodities. In positive macro-economics, we are widely worried about how national income and employment levels, total consumption and general level of investment and prices are determined. In these parts of positive economics, what should be the value, what the savings rate should be, what resources should be allocated and what the distribution of income should be.

Considering the perception of maximizing profits, this question, according to the question of what is, and what should be, in the scope of economics of norms, positive economics states that monopoly will determine a price which is equal to marginal cost with marginal revenue. The question is whether the price should be decided so that maximum social welfare can be achieved outside the scope of positive economics.

It is generally agreed that economics is both a positive and an ideal science. Economists believe that absolute neutrality between the ends is neither appropriate nor desirable. This is not possible because in many cases economists suggest ways to achieve some financial objectives. They advocate various policies for increasing employment, reducing inflation and so on. While making these suggestions, they are making a price decision.

Question 5.

How is micro economics different from macro economics? Write four sentences.

Answer:

The differences between micro and macro-economics are given below:

| Micro economics | Macro economics |

| (i) Micro economics studies economic relationships or economic problems at the level of an individual, an individual firm, an individual household or an individual consumer. | Macro economics studies economic relationships or economic problems at the level of the economy as a whole. |

| (ii) Micro economics is basically concerned with determination of output and price for an individual firm or industry. Accordingly, micro economics is briefly referred to as the theory of price. | Macro economics is basically concerned with determination of aggregate output and general price level in the economy as a whole. Accordingly, macro economics is briefly referred to as the theory of income and employment. |

| (iii) Study of micro economics assumes that macro variables remain constant, e.g., it is assumed that aggregate output is given while we are studying determination of output and price of an individual firm or industry. | Study of macro economics assumes that micro variables remain constant, e.g., it is assumed that distribution of income remains constant when we are studying the determination of aggregate output and income level. |

| (iv) Market mechanism plays a significant role in the context of micro economic problems, like the problem of product pricing Or factor pricing. | Government plays a significant role in the context of macro economic problems like the problems of unemployment, poverty and inflation. |

Question 6.

Discuss the difference between capitalist and socialist economics.

Answer:

The difference between capitalist and socialist economics is given below:

|

Capitalist Economy |

Socialist Economy |

|

(i) Economic resources are owned by private individuals. The right to own private property exists. |

All economic resources are owned by the State. The right to own private property is absent. |

|

(ii) Producers, resources owners and consumers are free to take economic decisions relating to production, allocation of resources and consumption respectively. |

There is loss of economic freedom with regard to consumers’ choice and allocation of resources by individuals. |

|

(iii) Price mechanism is allowed to operate freely. |

Price mechanism is not allowed to operate freely. |

|

(iv) Pricing or market mechanism is the basic coordinating mechanism. All economic decisions are taken through pricing mechanism. |

Planning takes the place of market mechanism. All important economic decisions are taken by the central planning authority. |

|

(v) Maximization of profit is the principal objective of producers. |

Maximization of social welfare is the chief motivating force behind all economic activities. |

|

(vi) Competition is an essential part of a capitalistic economy. |

Competition of all types is eliminated in a socialistic economy. |

|

(vii)Minimum intervention by the government. |

State regulated economy. |

|

(viii) Concentration of economic power in the hands of the capitalist class. |

Concentration of economic and political power in the hands of the government. |

|

(ix) There exist large inequalities in the distribution of income and wealth. |

It is based on the principle of egalitarianism. |

|

(x) There exists class struggle among various groups. |

It aims at establishing a classless society. |

Question 7.

What are the merits and demerits of mixed economy?

Answer:

Merits of a Mixed Economy

A mixed economy possesses the following merits:

(i) Proper Allocation of Resources : Economic planning ensures that economic resources of the economy are used in the best possible way.

(ii) Economic Stability : A mixed economy ensures economic stability. It tries to avoid fluctuations in the economy through planning and state regulation. It eliminates over¬production and under-production.

(iii) Advantages of the Market System : The system of mixed economy has all the advantages of both capitalist and socialist economies. It retains most of the institutions of capitalist economy by maintaining private property, inheritance rights, competition, profit motive, value system, independence of enterprise, private initiative, etc.

(iv) Rapid Economic Growth : From the perspective of the underdeveloped economies, the mixed economy pattern is important because it ensures faster economic growth. Mixed economy uses combined resources and energy of private resources and public communes to promote economic resources, achieved with social justice.

(v) Check the Concentration of Economic Power : A mixed economy is capable of examining the concentration of economic power: Monopoly control of industries and their exploitative tendencies are barred. Also, the inequality of government’s income is kept in check through the use of progressive taxation.

Demerits of a Mixed Economy

A mixed economy suffers from various shortcomings. The main drawbacks of mixed economy are given below:

(i) Conflict Between the Two Regions : One of the serious setbacks of mixed economy is that there can be a competition bitterness and non-co-operation between private and public sectors. In the case of mistrust and non-cooperation, the mixed economy may not work correctly.

(ii) Short term Nature : A mixed economy runs the risk of being short-lived. It cannot continue for a long time. During this time, each of the two areas could try to expand at the cost of each other. If the public sector extends to such an extent that it is able to acquire the private sector, the mixed economy can become a socialist economy.

(iii) Inadequate Operations : The risk of a mixed economy being driven in an inefficient way always esists. Due to excessive regulation and control of the government, the private sector has not been able to function effectively. On the other hand, the government sector is not working efficiently due to lack of initiatives from the bureaucrats and lack of responsibility.

(iv)Poor Performance of the Public Sector : In the mixed economy, the record of poor performance of the public sector makes the economic system suffer from inertia, inefficiency and red tapism. Experience of Indian economy testifies to this fact.

(v) Excessive Rules : A mixed economy is highly likely to give rise to a system of controls and rules. The government wants to regulate private sector by applying excessive control, licensing system, monetary and fiscal control. These excessive controls can be inconvenient, rigid and can promote economic inefficiency.

Quewstion 8.

What are the assumptions of production possibility curve? Mention the main characteristics of PPC.

Answer:

Assumptions of Production Possibility Curve

Production possibility curve is based on the following assumptions:

- The quantity of productive resources has been fixed.

- There is no change in technology.

- All productive resources are fully planned.

- Resources are not equally efficient in the production of all items. This means that the resources are transferred from one field to another, hence their production capacity decreases, thereby increasing the cost of production.

Characteristics of Production Possibility Curve

Production possibility curve has two characteristics:

(i) The Production Possibility Curve Slopes Downwards to Right: The possibility curve of the downward side yield indicates that the economy should drop some quantities of a good to achieve an additional amount of other good, assuming that resources have been given and used in the most effective way. Thus, when we go from combination B to C, the economy needs to give up 2 thousand guns to produce 1 million kg of extra butter. The reason for this is that additional resources are required to produce extra butter, which must be transferred from the production of guns.

(ii) It is Concave from the Origin : A concave shaped production possibility curve indicates increasing opportunity cost. The opportunity cost of a commodity (say butter) is the quantity of the other commodity (say guns), which need to be given up to get one unit of it. Thus, when we move from combination A to combination B, the economy has to give up 1 unit (thousand) of guns (15 – 14 = 1) to get 1 unit (million kg) of butter, and as we move from B to C, the economy is required to give up 2 units (thousands) of guns (14 – 12 = 2) to get 1 additional unit (million kg) of butter, and so on.

The reason for the increasing opportunity cost (real cost) is that resources are not equally efficient in the production of all goods. Therefore, as we transform more and more resources from the production of guns to the production of butter, we have to draw those resources which are more suited to the production of guns. Therefore, the quantity of guns sacrificed will increase.

Question 9.

What are the solutions to central problems in different economies?

Answer:

Different economies solve the central problems differently. Following are the details:

Market Economy : The market economy is an independent economy; it means that the producers are free to make decisions, on what basis do they make their decisions on ‘how and for whom?’ Yes, it is based on the value system. Producers choose to produce goods in which the prices are relatively high because they are interested in maximizing their revenue, they would like to adopt the production technology or would like to use those inputs, whose the price is relatively low. Because they are interested in reducing their costs. They will produce goods, and services for those buyers who are ready to provide them the maximum possible value, because they are interested in maximizing their profits.

Centrally Planned Economy : Decision relating to a centrally planned economy, is made by some central authority appointed by the government of the country, on ‘what, how and for whom’? and not on the basis of price mechanism.

All decisions are taken into account to maximize social welfare, and contrary to the market economy, maximization of profit is not considered. Those goods and services will be produced which the central authority (or government) finds most useful for the society. That technology of production will be adopted which is socially most useful. For example, in case of collective unemployment, labour-intensive technology will be given preference (rather than capital intensive technology) so that unemployment is low. Goods will be produced preferably for those residents who suffer from hunger or starvation, even when it involves incurring loss in production it.

Mixed Economy : Mixed economy combines the good qualities and avoids the flaws of market economy and centrally organized economies. Decision on the basis of price mechanism as well as on ‘what, how and for whom’ ? the goods are to be produced is based on social considerations. Such a situation can be described as the condition of ‘regulated price system’. In some areas of production, the producers are free to make their own decisions, while in other areas, decisions are taken entirely on the basis of social considerations. For example, In India, growers are free to produce cloth or steel to maximize their profits. But post and telegraph services are the monopoly of the government. The government provides these services at a nominal rate so that the poorest can afford them.

Question 10.

What is meant by economic growth? Differentiate between economic growth and economic development.

Answer:

Economic growth is generally defined as the process whereby real per capita income of a country increases over a long period of time. Economic growth has been defined in terms of national income aggregate. Everybody agrees that a necessary requirement of economic growth is an increased output of goods and services. Output is conveniently measured in terms of national income. It is with this idea that economic growth is defined in terms of national aggregates.

Unlike, economic growth, it is difficult to give a precise definition of economic development. Economic development is multi-dimensional in nature. Economists have defined economic development differently, depending upon which aspect of economic development they want to emphasize – output, distribution of income, standard of living, etc.

Economic development is the process whereby the real per capita income of a country increases over a long period of time, along with reduction of poverty, inequality and unemployment. It includes increase in income, reduction in economic inequality, improvement in material welfare, eradication of poverty, reduction of unemployment along with elimination of illiteracy, disease and early death.

Difference Between Economic Growth and Economic Development

The distinction between economic growth and economic development can be made on the following bases:

(i) Economic growth is a narrow concept, while economic development is a more comprehensive term. Economic development denotes growth plus change.

(ii) Economic growth refers to more output, resulting from use of more inputs and greater efficiency of inputs. Economic development goes beyond this to include composition of output, allocation of resources to different sectors of the economy like agriculture, industry, and bringing about structural changes.

(iii) Economic growth involves a rise in income. Economic development, on the other hand, involves not only rise in income, but also reduction of poverty, inequality of income and unemployment. .

(iv) Economic growth is defined strictly in terms of economic indicator, i.e., income. Economic development involves not only economic indicators, but also non-economic indicators like literacy, health services, etc.

(v) Economic growth is entirely a quantitative concept. Economic development involves not only quantitative, but many qualitative changes as well.

(vi) Economic growth is easier to realize. It is possible to increase output and income by using larger quantity of inputs and increasing their efficiency. The process of economic development is far more extensive. It involves a whole lot of changes in the society- changes in the social structure, attitudes, institutions as well as acceleration of economic growth, eradication of poverty and reduction of income inequalities. Therefore, attainment of economic development is a more difficult task.

(vii) Economic growth relates to the problems faced by the developed countries, while economic development relates to the problems faced by the present day developing countries.

(viii) Economic growth differs from economic development in terms of degree of involvement and intervention by the government. Economic growth does not require much of government intervention. However, economic development demands active involvement of the government. The government in the developing countries are expected to assume an active responsibility for promoting economic development.