Rajasthan Board RBSE Class 12 Economics Chapter 10 Equilibrium of a Firm

RBSE Class 12 Economics Chapter 10 Practice Questions

RBSE Class 12 Economics Chapter 10 Multiple Choice Questions

Question 1.

When TR is more than TC of a firm, then firm is getting :

(a) Abnormal Profit

(b) Loss

(c) No Profit, No loss

(d) None of these

Answer:

(a)

Question 2.

Point of profit is at:

(a) MR = MC

(b) TR = TC

(c)MR > MC

(d) MR < MC

Answer:

(c)

Question 3.

Loss to a firm is at:

(a) MR = MC

(b) TR > TC

(c) TR < TC

(d) TR = TC

Answer:

(c)

Question 4.

First condition of equilibrium is :

(a) MR = MC

(b) MR > MC

(c) MR < MC

(d) MR ≠ MC

Answer:

(a)

Question 5.

Firm determines the quantity of output where :

(a) MR = MC and MC cuts MR from below

(b) MR ≠ MC

(c) MR > MC

(d) MR < MC

Answer:

(a)

RBSE Class 12 Economics Chapter 10 Very Short Answer Type Questions

Question 1.

What do you mean by equilibrium of a firm?

Answer:

A firm is said to be in equilibrium when it has neither the tendency to increase, nor to reduce its level of output. At this output level, it maximizes its profits.

Question 2.

What is the point called, where TR = TC ?

Answer:

Break Even Point. At this point, the firm neither earns profit nor suffers loss.

Question 3.

What is marginal revenue?

Answer:

Marginal revenue means the addition made to the total revenue by selling an additional emit of the commodity.

Question 4.

How do you get Total Revenue?

Answer:

It is the total income of a company and is calculated by multiplying the quantity of goods sold by the price of the goods.

Question 5.

What is the state of firm when MR = MC ?

Answer:

This is the state of equilibrium of a firm where production quantity is optimum and profit is maximum.

RBSE Class 12 Economics Chapter 10 Short Answer Type Questions

Question 1.

Which method of finding equilibrium of firm (TR/TC or MR/MC) is superior and why?

Answer:

Both methods are used for finding the equilibrium of the firm. The TR / TC method is a simplified method whereas MR/MC method is considered as the best method because the quantity of production and maximum profit can be easily determined by it.

Question 2.

What do you mean by the Break-even point ?

Answer:

When both TR and TC are equal, then the firm neither earns any profit, nor suffers any loss. This stage is called the break-even point.

Question 3.

What are the two conditions for equilibrium of a firm by MC = MR method?

Answer:

Following are the two conditions for equilibrium of a firm by MC = MR method:

- The first and foremost condition of a firm’s equilibrium is that its MC should be equal to MR.

- MC Curve should intersect MR Curve from below, i.e., MC should be rising at the point of equilibrium.

Question 4.

What do you mean by total revenue and total cost?

Answer:

- Total Revenue – The amount of money received by the sale of an item by a firm is called total revenue. In the form of formula, Total Revenue = Quantity Sold × price (per unit).

- Total Cost – Total cost is the total expenditure on the production of certain quantity of a commodity.

In the form of formula, Total Cost = Total Fixed Cost + Total Variable Cost.

Question 5.

How does a firm attain maximum profit position ?

Answer:

The maximum benefit to a firm is at the production level where the difference between total revenue and the total cost is highest. It is the also the state of equilibrium of the firm. At this stage, the total cost is the lowest in comparison to total revenue and production level.

RBSE Class 12 Economics Chapter 10 Long Answer Type Questions

Question 1.

What do you mean by equilibrium of the firm ? Analyse the equilibrium of firm by MR = MC method with the help of diagram.

Answet:

A firm is in state of equilibrium, when it is earning maximum profit. The state of maximum profit occurs when the marginal revenue (MR) is equal to its marginal cost (MC).

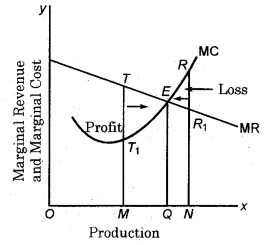

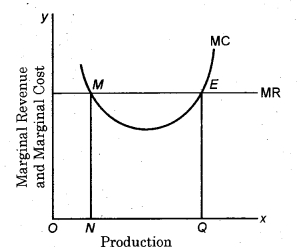

The point at which the marginal revenue and marginal cost are equal, before it, the marginal revenue is greater than the marginal cost. Thus, the firm will try to increase its profit further by increasing its production, but if more production is done beyond the equilibrium point, then MR exceeds MC, that is, total profit starts decreasing. Thus, no firm will want to move to this position. The best position for it will be where MR = MC. This can be clarified by the following figure –

In the above figure, production of commodity is taken along X axis, while the marginal revenue and marginal cost is shown along the Y axis.

MC is the marginal cost curve and MR is the marginal revenue curve. In monopolistic and imperfect competition markets, the MR curve slopes downwards, while marginal cost curve is U-shaped, because intially, marginal cost decreases upon increase in production, and later it keeps increasing.

The point E is the equilibrium point. Here, MR = MC. Hence, the quantity of production OQ is ideal, since at this point, firm’s profit is maximum.

If finn produces OM production less than OQ, marginal revenue (TM) is more than marginal cost (TM1). Thus, no producer would like to stop at this point. He will keep going beyond, till MR and MC become equal.

If firm increases its production from OQ to ON, then beyond point E, MC exceeds MR. This means, the firm is incurring losses from those additional units (QN) shown by an arrow. No firm will do this. Hence, the ideal state for the firm’s production is OQ where its profit is maximum.

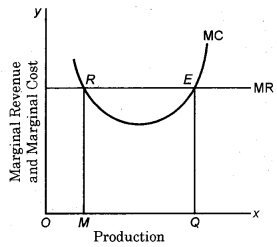

In a perfectly competitive market, along with the above condition, another condition has to be met for equilibrium of a firm; which is that marginal cost curve interesects marginal revenue curve from below. This can be clarified by the following figure –

In the above figure, E is the equilibrium point since both conditions of equilibrium are being met – (i) MR = MC (ii) MC curve cuts MR curve from below. This is the maximum profit state for the firm. In the figure, MR = MC at point R, but here, curve MC is cutting curve MR from above, hence it is not the firm’s equilibrium point and firm’s profit is not maximum at this point. If firm keeps its production less than OM, it will incur loss, since then MC exceeds MR. Similarly, if firm produces more than OQ, MC will again exceed MR, and total profit will decrease. Hence, its maximum profit will be at point E, the equilibrium point.

Question 2.

Using TR and TC method explain equilibrium of firm. Use figure.

Answer:

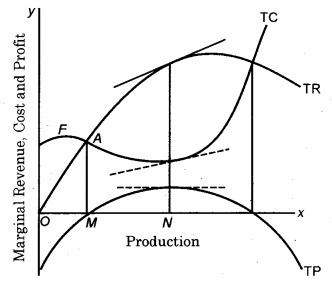

A firm is in equilibrium when it produces that amount of output at which the difference between total revenue (TR) and total cost (TC), i.e., total profit, is maximum. This situation is shown in the given figure:

The total revenue (TR) curve begins with the origin, which means that when there is no output, the revenue is zero. As the output grows, the total revenue is rising at a steady rate, the reason being that the price of the company working under the right competition remains

constant, depending on the level of production. Consequently, the total revenue curve (TR) is a straight line from the origin.

Total Cost (TC) curve starts from a point F which lies above the origin. It means that OF is the fixed cost which the firm has to incur even if it stops production for a short time. As the firm increases its production in the initial stages, the total cost is more than the total revenue and the firm is not making profits at all. When it produces OM level of output, total revenue just equals total cost, and the firm is, therefore, neither making profits nor losses.

That is, the firm is only breaking even at the output level OM. Thus, the point A or output level OM is called Break-Even-Point. When the firm increases its output beyond OM, total revenue becomes larger than total cost and profits begin to accrue to the firm. Profits are increasing as the firm increases production from output OM to output ON. Since the distance between the total revenue curve and total cost curve is widening, at ON level of output, the distance between the TR curve and TC curve is the greatest, and, therefore, profits will be maximum at point E.

RBSE Class 12 Economics Chapter 10 Other Important Questions – Answers

RBSE Class 12 Economics Chapter 10 Multiple-Choice Questions

Question 1.

At equilibrium price :

(a) Demand is more

(b) Supply is more

(c) Demand and supply are equal

(d) None of these

Answer:

(c)

Question 2.

If demand increases at a faster rate than the supply, equilibrium price will:

(a) Increase

(b) Decrease

(c) Neither increase nor decrease

(d) None of the above

Answer:

(a)

Question 3.

If demand and supply change at the same rates, the equilibrium price will:

(a) Remain constant

(b) Increase

(c) Decrease

(d) None of these

Answer:

(a)

Question 4

………………… a dominant role in determining equilibrium price in the short period:

(a) Demand plays

(b) Supply plays

(c) Demand and supply play

(d) None of the above

Answer:

(a)

Question 5

………………… a dominant role in determining equilibrium price in the long period:

(a) Demand plays

(b) Supply plays

(c) Demand and supply play

(d) None of the above

Answer:

(c)

Question 6

………………… a dominant role in determining market price :

(a) Demand plays

(b) Supply plays

(c) Demand and supply play

(d) None of the above

Answer:

(a)

Question 7.

The concept of equilibrium price is …………………

(a) Theoretical

(b) Practical

(c) Both

(d) Neither theoretical nor practical

Answer:

(a)

Question 8.

Traders enjoy ………………… profit at equilibrium price :

(a) Normal

(b) Abnormal

(c) Lesser

(d) More

Answer:

(a)

Question 9.

Market price is ………………… equilibrium price :

(a) More than

(b) Less than

(c) Equal to

(d) Either less or more than

Answer:

(d)

Question 10.

Slope of supply curve is …………………

(a) Positive

(b) Negative

(c) Both

(d) Parallel

Answer:

(a)

Question 11.

Secular price is fixed in the ………………… Period:

(a) Very short

(b) Short

(c) Long

(d) Very long

Answer:

(d)

Question 12.

Normal price is fixed in the ………………… period:

(a) Market

(b) Short

(c) Long

(d) Very long

Answer:

(c)

Question 13.

A firm is in a state of balance while :

(a) When it is in a position to reduce the production of the goods.

(b) When the production of the goods is in the condition of increasing.

(c) When the production of goods neither increase nor decrease.

(d) None of these

Answer:

(c)

Question 14.

Objective of all the firms is :

(a) Selling your item at cost price

(b) Earning maximum profit

(c) Social service

(d) None of these

Answer:

(b)

Question 15.

When the production is zero, then the total revenue is equal to :

(a) Zero

(b) Maximum

(c) Equal to Fixed Cost

(d) None of these

Answer:

(a)

RBSE Class 12 Economics Chapter 10 Very Short Answer Type Questions

Question 1.

What is meant by producer’s equilibrium?

Answer:

It is the situation in which the producer maximizes his profit or minimizes his loss.

Question 2.

What is meant by Equilibrium of the firm?

Answer:

A firm’s equilibrium is a level of output at which a firm either maximizes its profits or minimizes its losses.

Question 3.

What are the conditions for the producer’s equilibrium?

Ans.

To maximize his profit, a producer will produce upto that quantity at which the following two conditions are fulfilled:

- Marginal Revenue (MR) = Marginal Cost (MC)

- MC should be rising after that point of production.

Question 4.

What is gross profit?

Answer:

The difference between total revenue and total variable cost is called gross profit. It is calculated like this : Gross Profit = TR – TVC

Question 5.

What is net profit?

Answer:

TR – (TVC + TFC) = Net Profit.

Question 6.

Under what market conditions a firm is a Price-taker?

Answer:

Under Perfect Competition market conditions, a firm is a Price-taker.

Question 7.

Find firm’s equilibrium with the help of total revenue and total cost curves.

Answer:

A firm is in equilibrium when it produces that amount of output at which the difference between total revenue(TR) and total cost (TC), i.e., total profits, is maximum.

Question 8.

Find firm’s equilibrium with the help of marginal revenue and marginal cost curves.

Answer:

Profit will be highest at that level of output where marginal cost coincides with the marginal reveue, i.e., MC = MR.

Question 9.

Normal profits are part of average cost. Discuss.

Answer:

Normal profits are part of average cost because in this situation average revenue (AR) is equal to average cost(AC) and average revenue is called normal profit. This is the position of equilibrium.

Question 10.

What do you understand by equilibrium of an industry?

Answer:

An industry is in equilibrium at a price and output at which its market demand equals its market supply.

Question 11.

Mention the concept of shut-down point.

Answer:

The last price at which a firm will continue to operate must be equal to the average variable cost. This point is known as the shut-down point.

RBSE Class 12 Economics Chapter 10 Short Answer Type Questions

Question 1.

Discuss the conditions Of equilibrium of an industry.

Answer:

There are two conditions of a firm’s equilibrium which we discuss below:

- Equality of MR and MC. A firm will be in equilibrium when it is earning maximum profits.

- MC curve must cut MR curve from below at the equilibrium point.

Question 2.

Point out the main difference between the equilibrium of a firm and an industry.

Answer:

The main difference between the equilibrium of a firm and an industry is the following:

- Industry is a group of firms which are producing a homogeneous product.

- An industry is in equilibrium when all the firms are operating and no new firm enters the market or no existing firm leaves the industry.

- Industry equilibrium is determined by conditions of demand and supply. The industry will be in the condition of equilibrium when all firms are in equilibrium, no new firms enter and no old firms leave the industry.

- Industry will be in the position of equilibrium in the long run because all the possible adjustments can be made. Long run equilibrium of an industry is more stable.

Question 3.

Why does a firm earn maximum profits by producing the amount of output where marginal revenue is equal to marginal cost?

Answer:

Profits will be highest at that level of output where marginal cost coincides with the marginal revenue, i.e., MC = MR. A firm will go on expanding its level of output so long as an extra unit of output adds more to revenue than to cost. Since it will be profitable to do so. The firm will not produce an additional unit of the product which adds more to cost than to revenue because to produce that unit will mean losses. Thus, a firm will go on expanding output as long as marginal revenue (MR) exceeds marginal cost (MC) of Production. The level of output where marginal revenue (MR) and marginal cost (MC) equals is the point of maximum profit.

Question 4.

What do you understand by total revenue of the firm?

Answer:

According to Dooley, “Total revenue is the sum of all sales, receipts or income of a firm.”

According to Clower and Due, “Total revenue may be defined as the product of planned sales (output) and expected selling price.”

Question 5.

If you are an entrepreneur and working under conditions of perfect competition, when would you decide to shut down in the short-run?

Answer:

Under perfect competition, we would decide to shut down in the short-run when the marginal revenue drops below the average variable cost. In case price falls below this point, then firm will not even be able to meet its average variable cost. It will constitute more than minimum loss, and to avoid it, the firm will prefer to shut down its production. Thus, shut down price is the price below which the firm chooses not to produce at all.

Question 6.

Write down two features of perfect competition.

Answer:

Following are the two features of perfect competiton

- A Large Number of Firms The first condition of perfect competition is that there are a large number of companies in the industry. The presence of a large number of firms making and selling the product ensures that no single producer or buyer can have any effect on the price of the product.

- Homogenous Product The products produced by all firms in the industry are fully homogeneous and identical. It means that the products of various firms are indistinguishable from each other; they are perfect substitutes for one another. The control over price is completely eliminated only when all firms are producing homogeneous products.

Question 7.

What do you mean by Long-run equilibrium of firm?

Answer:

There is a long term period, which is long enough to allow the firm to make changes in all the factors of production. In the long run, all the factors are variable. Economics has not been a definitive factor for a long time in that period. Every factor can be changed, the size of the firm can change, a new company can enter the industry or old companies can leave it. In this way, long-term supply can be fully adjusted with demand.

Question 8.

What do you mean by Short-run period in equilibrium of firm?

Answer:

Short term is the period of time in which companies can change or decrease the number of step factors such as labour and raw materials only, while there is no change in certain factors such as capital equipment. In addition, in the short term, new companies cannot enter the industry, nor can the existing firms leave.

Question 9.

What is Total Revenue-Total Cost approach?

Answer:

A firm is in equilibrium when it produces that amount of output at which the difference between total revenue (TR) and total cost (TC), i.e., total profit is maximum. A producer can earn maximum profits when difference between TR and TC is maximum. By fixing different prices, a producer tries to find out the level of output where the difference between TR and TC is maximum. The level of output where producer earns maximum profits is called the equilibrium situation.

Question 10.

What is Marginal Revenue and Marginal Cost approach?

Answer:

According to marginal revenue and marginal cost approach, a producer will be in equilibrium when two conditions are fulfilled i.e., (i) MC=MR and (ii) MC must cut MR from below. This is a better method to analyse the equilibrium point of a firm, since both optimum production and total profit can be easily determined by it.

Question 11.

What is the meaning of equilibrium of industry under perfect competition?

Answer:

An industry is in equilibrium at a price and output at which its market demand equals its market supply. When an industry is in equilibrium, all its firms are supposed to be in equilibrium, and earn only normal profits. This is so because under the conditions of perfect competition, all the firms are assumed to achieve the same level of efficiency in the long-run. Since industry yields only normal profits, there is no incentive for new firms to enter the industry, or existing ones to leave it.

Question 12.

What do you understand by Break-even point in equilibrium of firm?

Answer:

Break-even for a firm occurs when it is able to cover all its costs of production. Under this situation, the firm earns only normal profit, i.e. neither super normal profits nor super normal losses. This situation prevails at the point where Total Cost is equal to Total Revenue, i.e. TR = TC or AR = AC.

Question 13.

What is meant by equilibrium price and production ?

Answer:

Equilibirum price and production implies that quantity at which the firm earns highest profit. Above and below this point, the production and price both are not optimum to maximise the firm’s profit.

Question 14.

Mention the drawbacks of total revenue – total cost method.

Answer:

Following are the drawbacks –

(i) It is difficult to determine the maximum distance between total revenue and total cost.

(ii) It is not possible to determine the per unit cost on basis of diagram.

Question 15.

Show the equilibrium position through a diagram, using the marginal revenue-marginal cost method.

Answer:

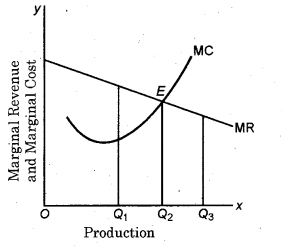

Equilibrium position by marginal revenue and marginal cost method :

‘E’ is the equilibrium point, and OQ is equilibrium quantity. At point E, MR = MC.

Question 16.

How is the highest difference between total cost curve and total revenue curve found out ?

Answer:

To know highest the difference between TR and TC curves, tangents are drawn on both curves. The points at which these tangents touch the curves, the distance between them is the highest difference between TR and TC. Hence at this production level, the profit is also the highest.

RBSE Class 12 Economics Chapter 10 Essay Type Questions

Question 1.

Perform a comparative analysis between the total cost—total revenue method and marginal cost-marginal revenue method of finding a firm’s equilibrium point.

Answer:

Two methods are used to determine the equilibrium point of a firm—

(i) Total revenue – Total cost method

(ii) Marginal revenue – Marginal cost method

The Total cost – Total revenue method is a simple and logical method. Most firms use this method, but it has certain defects :

(i) It is difficult to determine the greatest distance between total revenue and total cost. The real point is determined by drawing many tangents.

(ii) It is not possible to find the per unit cost of the commodity on basis of the. diagram, since the cost diagram cannot be directly shown.

The marginal revenue and marginal cost method is considered to be superior, because it is easy to determine the maximum profit and production quantity (optimum) using this method. Per unit cost can also be determined by using the average revenue and average cost curves of the firm.

Question 2.

How is the equilibrium of a firm determined in a perfect competition state ? Explain with the help of a diagram.

Answer:

Perfect competition is that state of the market in which the price of a commodity is determined on the basis of total demand and supply of the industry. In this condition, each firm has to sell its commodity at that very price. Firm is not a price determiner but a price accepter. Hence, the marginal revenue curve of the firm in this situation is a straight line parallel to the X axis.

The marginal cost curve is a perfect U-shaped curve in perfect competition market as it is in any other market, since it is affected by laws of production.

In a perfect competition market, the firm’s equilibrium lies at a point, where the following two conditions are met –

- Where marginal revenue (MR) is equal to marginal cost (MC).

- Where the marginal cost curve cuts the marginal revenue curve from below.

This can be shown by the following figure :

Explanation of the figure :

At point E, the marginal revenue (MR) is equal to the marginal cost (MC). Also at this point, the MC curve cuts the MR curve from below. Hence, both conditions of equilibrium are being fulfilled at this point. This is the firm’s equilibrium point and OQ is the equilibrium quantity.

In contrast, if the firm produces equal to ON, the first condition of equilibrium, since marginal revenue is equal to marginal cost, but the second condition is not fulfilled, because at this point the marginal cost curve is not cutting the marginal revenue curve from below. Hence, the firm cannot earn maximum profit at this point. Thus, this is not a state of equilibrium.

RBSE Class 12 Economics Chapter 10 Numerical Questions

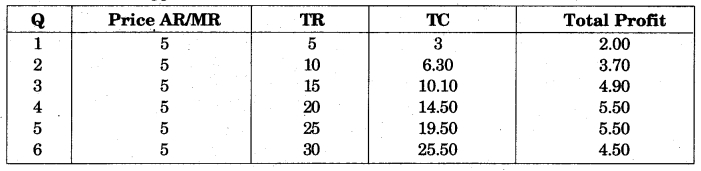

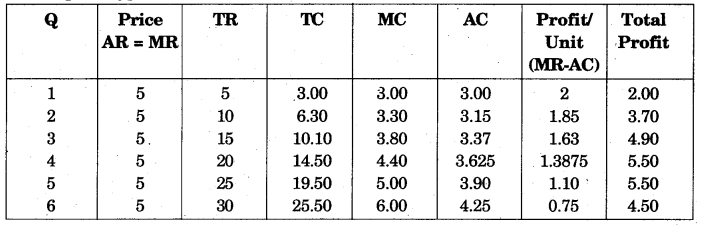

Question 1.

Assuming the prevailing market price to be ₹ 5 per unit, the cost and production data of a hypothetical firm is presented in the following Table.

Show numerically with (a) the total cost approach, (b) marginal approach, the best level of output when the total profit of the firm would be maximum.

Solution :

(a) Total Cost Approach

It is obvious from the table that profits are maximized (at ₹ 5.50) when the firm produces and sells 5 units of the commodity per time period.

(b) Marginal Approach

The best level of output would be 5 units, because at this Point, output MR = MC. The firm’s profit is maximum ( ₹ 5.50).

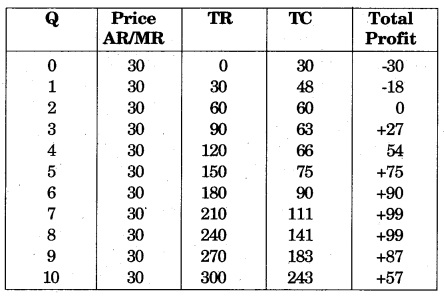

Question 2.

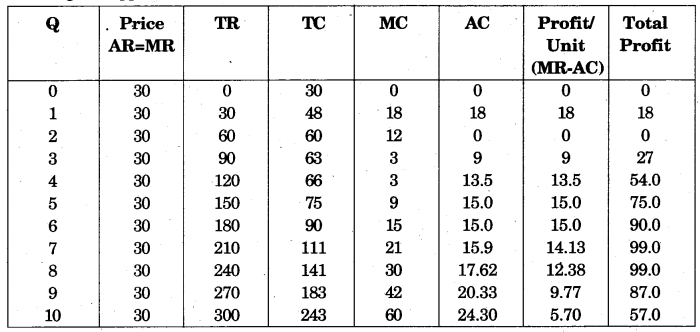

From the following table find out the level of output at which the firm will earn maximum profit supposing the market price of commodity in the market to be ₹ 30.

Solution :

(a) Total Cost Approach

Total profits are maximum ( ₹ 99) when the firm produces and sells 8 units of the commodity,

(b) Marginal Approach

By marginal approach also, we find that the best level of output would be 8 units because at this output both the MR and MC are ₹ 30. Hence, the firm’s profit is maximum ( ₹ 99).

Question 3.

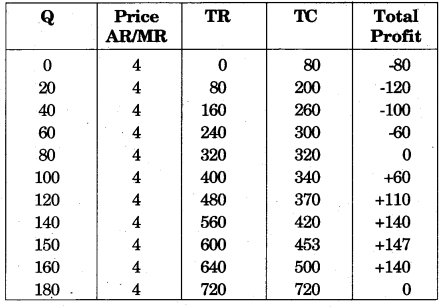

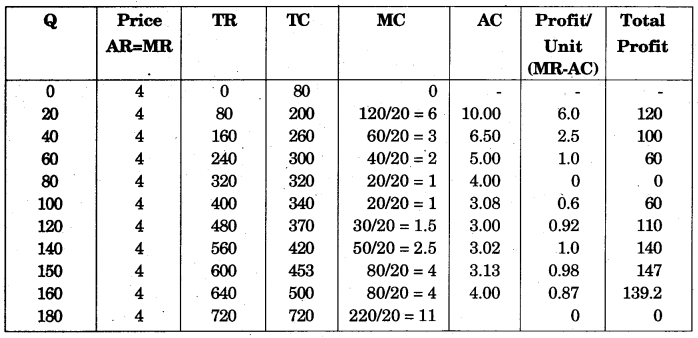

Assuming the prevailing market price to be ₹ 4 per unit. The cost and production data of a hypothetical firm is presented in the following Table.

Show with (a) the total cost approach, and (b) marginal approach the best level of output at which the total profit of the firm would be maximum.

Solution :

(a) Total Cost Approach

It is obvious from the table that total profit is maximized (at ₹ 147) when the firm produces and sells 150 units of the commodity per time period.

(b) Marginal Approach

The MC of ₹ 4 at 150 units of output was obtained by finding the change in TC per unit increase in output, when output is increased from 140 units to 160 units.