Rajasthan Board RBSE Class 12 Economics Chapter 13 Market Equilibrium

RBSE Class 12 Economics Chapter 13 Practice Questions

RBSE Class 12 Economics Chapter 13 Multiple Choice Questions

Question 1.

Relation between price and market demand for a particular good is :

(a) Positive

(b) Negative

(c) Zero

(d) No relation

Answer:

(b)

Question 2.

At equilibrium price, satisfaction is gained by :

(a) Buyer and seller both

(b) Only buyer

(c) Only seller

(d) Neither buyer nor seller

Answer:

(a)

Question 3.

Main cause for demand of a commodity is :

(a) Supply of money

(b) Supply of goods

(c) Attribute of want satisfying capacity

(d) Availability of goods

Answer:

(c)

Question 4.

A producer produces an object with the aim of :

(a) Social service

(b) Self satisfaction

(c) To earn profit

(d) To achieve prestige

Answer:

(c)

Question 5.

Due to increase in supply of a product, the supply curve:

(a) Shifts to the right

(b) Shifts to the left

(c) Remains constant

(d) No change

Answer:

(a)

RBSE Class 12 Economics Chapter 13 Very Short Answer Type Questions

Question 1.

Give the definition of equilibrium as given by Prof. J.K. Mehta.

Answer:

According to Prof.J.K. Mehta, “Equilibrium denotes a state whose feature is lack of change.”

Question 2.

Price of a commodity is determined by which two factors?

Answer:

Demand and Supply of the product.

Question 3.

What do you mean by market equilibrium? Explain.

Answer:

Market equilibrium is a situation of the market in which demand for a commodity in the market exactly matches its supply corresponding to a particular price.

Question 4.

What do you mean by market demand? Explain.

Answer:

Market demand is the sum total of quantities which are demanded by various consumers at a certain price in the market.

RBSE Class 12 Economics Chapter 13 Short Answer Type Questions

Question 1.

Write down any three elements which affect the supply of a commodity.

Answer:

Following are the three elements which affect the supply of a commodity:

(a) Supply changes when the cost of production changes. When cost increases, supply decreases, and when cost decreases, then supply increases.

(b) Supply is affected by new inventions. When the use of new replacement goods increases then the supply of old goods decreases.

(c) Technological changes affect supply of a product through changes in production level.

Question 2.

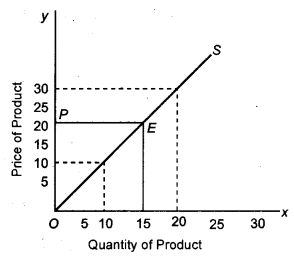

Show supply curve diagrammatically.

Answer:

Question 3.

What is supply schedule?

Answer:

A producer is ready to sell different quantities of his goods at different prices at a certain time, which is called its supply schedule. The market supply schedule is obtained on totalling supply schedules of all the producers of the market.

RBSE Class 12 Economics Chapter 13 Essay Type Questions

Question 1.

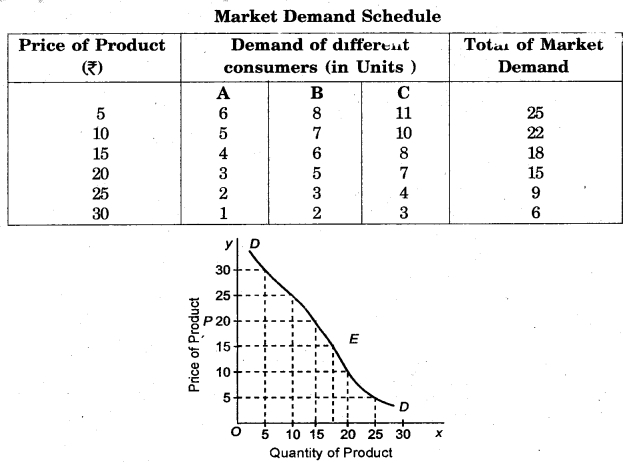

Construct a hypothetical market demand schedule. Explain it with the help of figure.

Answer:

Demand schedule for different items at different prices is also different. Each buyer has a demand schedule. Market demand schedule is available on the use of demand schedule for all buyers in the market. We can understand this from the following imaginary table –

In the above diagram, the quantity of the product is shown on the X axis and the price of the product is shown on the Y axis. The sum total of the demands of all consumers has been expressed by the market demand, in which the quantity of OQ expresses demand of the product at OP price. When the price of the product increases, the demand for the product decreases. DD demand curve showing the demand of the product at different price levels expresses the market. The negative slope of the demand curve reflects the trend of demand in the market.

Question 2.

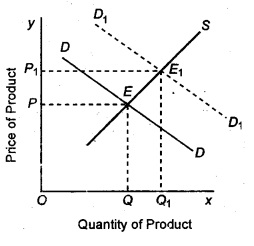

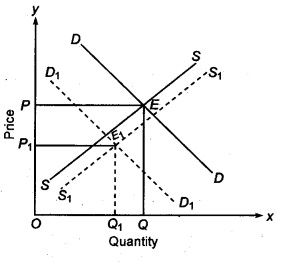

Due to change in demand, equilibrium price changes”. Explain this statement diagrammatically.

Answer:

Changes in demand affects equilibrium price – Demand for any item can be changed by consumers’ interest, income, temperament, fashion, preference, time effect, etc. When the supply of any. object and other circumstances remains stable, but if the demand for the object increases due to any reason, the equilibrium will also be affected, and both the equilibrium price and quantity will increase, whereas on the contrary, the demand for the goods, due to any reason, decreases, it is clear that if the supply is unchanged, the price of the item and the sale quantity both decrease decrease.

(i) Effect of increase in demand – It is clear that the intersection of demand and supply is initially at E. Equilibrium price is OP and equilibrium quantity is OQ. Now due to increase in demand, demand curve shifts upward to D1D1 and new equilibrium is at E1 Therefore, new equilibrium point is E1 new equilibrium price is OP1 and equilibrium quantity is OQ1

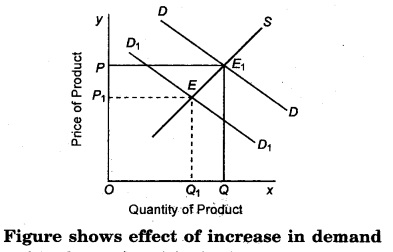

(ii) Effect of decrease in demand – It is clear from the figure that equilibrium once established, changes due to decrease in demand. If due to any reason, demand decreases, then demand curve will shift downwards and the new demand curve will be at D1D1. Here, supply curve SS and new demand curve D1D1 intersect at E1 Therefore, new equilibrium price is OP1 new quantity is OQ1 In this way, due to decrease in demand, market price comes down and equilibrium quantity decreases from OQ to OQ1.

Question 3.

Discuss demand and supply with the help of schedule and figure.

Answer:

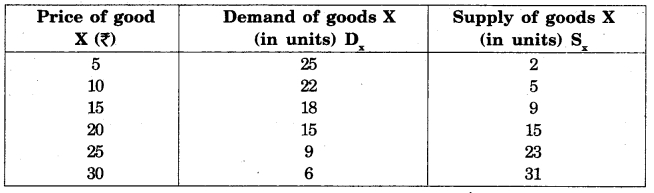

Equilibrium of Deaihand and Supply – From analysis of demand side, it is clear that marginal utility of a product is the highest limit of its price, and from analysis of supply curve, it is clear that its marginal cost is lower limit of its price. Therefore, actual price is determined in between these two limits. The price is determined where Dx = Sx. Buyer is interested to pay as minimum as possible and seller wants to charge maximum price. Therefore, price determined at this point is equilibrium price” and quantity is “equilibrium quantity”.

Explanation of Table – It is clear from table that as price increases, quantity demanded decreases, whereas supply increases. In table, it is clear that at price ₹ 20, Quantity demanded (Dx) = Quantity supplied (Sx). Therefore, equilibrium price = ₹ 20 and equilibrium quantity = 15 units.

Explanation of the Figure :

Figure shows that on X axis, units of demand and supply are taken, and on Y axis, price of goods X has been taken. DD is the demand curve and SS is the supply curve. Demand and supply curve intersect at point E.

Therefore OP is price and OQ is the quantity demanded and supplied. Price determined at E is equilibrium price. When price of commodity X is ₹ 20, then Qd = Qs = 15 Units. Therefore, E is equilibrium point where Qd = Qs.

Question 4.

Analyse market equilibrium. What is the effect of change in supply on its equilibrium? Explain.

Answer:

Market equilibrium is a situation of the market in which demand for a commodity in the market exactly matches its supply corresponding to a particular price, called equilibrium price. Thus, in a state of equilibrium, the market clears itself as market demand = market supply of the commodity. There is neither excess demand nor excess supply. In such a situation, the price that prevails in the market is called equilibrium price. It is called general theory of price determination or price determination theory of demand and supply. Marshall assumes that price of a commodity is neither determined by demand (utility) nor supply of the commodity (cost of production), but it is rather determined by the forces of both – demand and supply.

Effect of changes in supply on Equilibrium

Supply of any commodity may change due to various factors. The main ones are:

- Supply may change due to changes in cost of production. With increase in cost, supply decreases, and with decrease in cost, supply will increase.

- New inventions also affect the supply of a product. Due to increased use of new substitutes, the price and supply of old goods decreases.

- Technological change also changes the level of production. This results in change in supply.

- Discovery of new sources of raw material increases the supply of goods.

- Changes in the attitude of producer also changes supply.

- Changes in government policy may also change the supply.

RBSE Class 12 Economics Chapter 13 Other Important Questions – Answers

RBSE Class 12 Economics Chapter 13 Multiple-Choice Questions

Question 1.

What are the causes of origination of excess demand?

(a) Increase in supply of currency

(b) Increase in public expenses

(c) Increase in taxes

(d) None of these

Answer:

(d)

Question 2.

According to which of the following, the price of any product is determined by the forces of both demand and supply?

(a) Walrus

(b) Marshall

(c) Hicks

(d) Benham

Answer:

(b)

Question 3.

Equilibrium price is equal in the perfect competitive market –

(a) to equilibrium quantity

(b) to total receipt

(c) to total cost

(d) to minimum average cost

Answer:

(c)

Question 4.

Word ‘equilibrium’ is of which language –

(a) Italian

(b) French

(c) Latin

(d) Babylonian

Answer:

(c)

Question 5.

What is the meaning of equilibrium?

(a) Stability

(b) Unchangeability

(c) Mobility

(d) All of these

Answer:

(b)

Question 6.

What is the effect on the price if the supply of a product increases ?

(a) Increases

(b) decreases

(c) No effect

(d) None of these

Answer:

(b)

Question 7.

What is the impact on the price if the supply of a product decreases?

(a) Increases

(b) decreases

(c) No effect

(d) None of these

Answer:

(a)

Question 8.

The relation between the price and demand of a product is :

(a) Positive

(b) Negative

(c) Equal

(d) None of these

Answer:

(b)

Question 9.

The slopes of the Market demand curve of a product is :

(a) Positive

(b) Negative

(c) Straight

(d) None of these

Answer:

(b)

Question 10.

When the price of any product increases, its demand :

(a) Increases

(b) Decreases

(c) No effect

(d) None of these

Answer:

(b)

RBSE Class 12 Economics Chapter 13 Very Short Answer Type Questions

Question 1.

What do you mean by equilibrium?

Answer:

Equilibrium is the situation in which the total market supply is equal to total market demand.

Question 2.

What is the meaning of excess supply?

Answer:

When the market supply is more than the market demand at a certain price (S > D).

Question 3.

What do you mean by excess demand?

Answer:

When the market demand is more than the market supply at a certain price (S<D).

Question 4.

What is the meaning of equilibrium price?

Answer:

The price at which the equilibrium is established is called the equilibrium price.

Question 5.

What do you mean by equilibrium demand?

Answer:

The quantity of a product sought at the equilibrium price is called equilibrium demand.

Question 6.

What is the condition of demand and supply at any other point in place of equilibrium point?

Answer:

There may be a demand surplus or a supply excess at any point other than the equilibrium point.

Question 7.

What is the slope of market demand curve?

Answer:

Negative.

Question 8.

What is the slope of market supply curve?

Answer:

Positive.

Question 9.

Write down one characteristic of market.

Answer:

In the market, goods, services and resources are sold and bought.

Question 10.

What is the objective of firms in a perfect competitive market?

Answer:

Profit maximization.

Question 11.

What is the impact of an increase in the price of an input on its demand?

Answer:

When the price of an input increases, its demand decreases.

Question 12.

If the supply of a product is perfectly elastic, then tell the effect of the increase in the demand of the object on the price and quantity of the product.

Answer:

In this situation, price of product is not affected, whereas its quantity increases.

Question 13.

If the supply of the product is perfectly inelastic, then what will be the effect on the price and quantity of the product when the demand for the item increases?

Answer:

Price of the product increases, but its quantity is not affected.

Question 14.

If the supply of the product is perfectly inelastic, then what will be the effect on the price and quantity of the product, when the demand of item decreases?

Answer:

Its equilibrium price decreases, but the quantity of the product is not affected.

Question 15.

If the demand is perfectly elastic, then what will be the effect on its equilibrium price and quantity, when the supply of object decreases?

Answer:

Price is not affected, but the quantity increases.

Question 16.

If the demand of a product is perfectly elastic, then what will be the effect on its equilibrium price and quantity, when the supply of the product increases?

Answer:

The product’s price is unaffected, but its quantity increases.

Question 17.

If the demand of a product is perfectly inelastic, then what will be the effect on its equilibrium price and quantity, when the supply of object increases?

Answer:

Quantity of product is not affected, but its price reduces.

Question 18.

When the market supply is more than market demand, then what will this condition be called?

Answer:

Excess Supply.

Question 19.

When the market demand is more than market supply, then what will this condition be called?

Answer:

Excess Demand.

Question 20.

If both, the market demand and supply curves are shifted to left, then what will be the effect on equilibrium quantity?

Answer:

Equilibrium quantity decreases.

Question 21.

If both, the market demand and supply curves are shifted to the right, then what will be the effect on equilibrium, quantity?

Answer:

Equilibrium price increases.

Question 22.

In the event of uninterrupted entry and exit of firms in a market, what will be the price in the perfectly competitive market?

Answer:

Equal to minimum average cost.

Question 23.

What is the condition of market demand and supply in the condition of equilibrium of market?

Answer:

Market demand and Market supply are equal to each other.

Question 24.

Who demands the goods in the merchandise market?

Answer:

Goods are demanded by families.

Question 25.

Who supplies the goods in the merchandise market?

Answer:

Goods are supplied by the producing firms.

Question 26.

What are the two causes of increase in supply in market?

Answer:

- Improvement in technology

- Decrease in production input prices.

Question 27.

What are the two causes of decrease in supply in market?

Answer:

- Price of goods

- Cost of the means of production.

Question 28.

What will be the equilibrium in the condition of uninterrupted entry and exit, if the market demand curve q0 = 200-P and equilibrium price (P) = 10.

Answer:

Equilibrium Quantity (q0) = 200 – P

= 200 – 10

= 190.

Question. 29.

What do you understand by Rationing?

Answer:

Determination of the highest quantity of consumption of a product by a person is known as rationing.

Question 30.

What will be the effect on demand of labour when the price of product increases?

Answer:

Demand of labour increases.

RBSE Class 12 Economics Chapter 13 Short Answer Type Questions (SA-I)

Question 1.

Explain the status of zero excess demand and zero excess supply.

Answer:

When market demand and market supply at a particular price are equal, it is called the status of zero excess demand and zero excess supply.

Question 2.

What does the market demand curve’reflect?

Answer:

Market demand curve reflects that quantity of commodity which every consumer wishes to purchase at different prices.

Question 3.

What does the market supply curve reflect ?

Answer:

Market supply curve reflects that quantity of commodity which every firm wishes to supply at different prices.

Question 4.

What is the effect on the equilibrium price when there is an increase in the price of the substitute good?

Answer:

Increase in the price of the substitute good, increases the amount of demand of the substitute good, so that the equilibrium price of that good increases.

Question 5.

What do you understand by controlled price?

Answer:

Setting the price at a level below lower than the equilibrium price, so that the availability of the goods can be ensured for the poor classes.

Question 6.

What does support price mean?

Answer:

To protect the well-being of farmers, determining the price of a product at a higher level than the equilibrium price is called support price.

Question 7.

What does the market price mean?

Answer:

The price which is determined by the relative forces of demand and supply, and which keeps changing from time to time.

Question 8.

What is the meaning of normal price?

Answer:

The price of a product that is found in the long run, and the equilibrium of demand and supply in it is fixed.

Question 9.

What is the difference between demand and supply curves of a commodity market?

Answer:

The demand curve of the goods in a commodity market is falling down, while the supply curve is rising up.

Question 10.

Clarify the meaning of equilibrium in an industry.

Answer:

When the total supply of the product produced by the industry at a given price equals its total demand, the industry is in the state of equilibrium.

Question 11.

Find out the equilibrium price, when the market demand curve QD = 200 – P and supply curve Qs = 120 + P.

Answer:

Equilibrium Price QD = Qs

200 – P = 120 + P

2P = 200 – 120

P = 80/2

P = ₹ 40.

Question 12.

Find out the quantity of equilibrium, if market supply curve Qs = 140 + P and price of equilibrium P = ₹ 20.

Answer:

Qs = 140 + P

P = 20

= 140 + 20

Qs = 160

Question 13.

What do you understand by Maximum Fixed Price?

Answer:

The upper limit set by the government of the price of any product or service is called the Maximum Fixed Price.

Question 14.

What do you understand by Minimum fixed Price?

Answer:

The lower limit set by the government of the price of any product or service is called the Minimum Fixed Price.

Question 15.

If the government imposes a tax on a commodity in the market, how will it affect the equilibrium price?

Answer:

If the government imposes a tax on a commodity in the market, then the equilibrium price will increase.

Question 16.

Write down one difference between equilibrium price and control price.

Answer:

The control price is determined by the government, while equilibrium price is determined by the forces of demand and supply in the market.

Question 17.

What do you understand by Black Marketing ?

Answer:

Selling a product illegally at a price higher than the price fixed by the government is called black marketing.

Question 18.

What is the difference between the price and quantity of commodity?

Answer:

Both have an inverse relationship. When the price increases, the quantity of the item decreases, and the quantity increases, when the price decreases.

Question 19.

What are the types of government interferences in an economy?

Answer:

There are two ways in which government interferes in an economy –

- Directly

- Indirectly.

Question 20.

If there is a decrease in both demand and supply, then what will be the impact on equilibrium price?

Answer:

The price will remain stable due to lack of normal conditions in both demand and supply. If demand is lesser than supply, then there will be a decrease in price, and if the Supply is less than demand, then the price will increase.

Question 21.

What will be the effect on the equilibrium price when the demand quantity is increased and there is a decrease in the supply quantity of the same goods?

Answer:

If the commodity’s demand quantity increases and its supply quantity decreases, then its equilibrium price increases.

RBSE Class 12 Economics Chapter 13 Short Answer Type Questions (SA-II)

Question 1.

What does equilibrium mean? In which situation is the market said to be in a state of equilibrium?

Answer:

The market condition in which there is no tendency for change of any kind is called the state of equilibrium. In the state of equilibrium, both demand and supply are equal.

Market equilibrium : is that state of market, in which total market supply is equal to the total market demand.

Qs = Qd [Where Qs = total market supply; Qd = total market demand]

Question 2.

Explain market equilibrium through a table and diagram.

Answer:

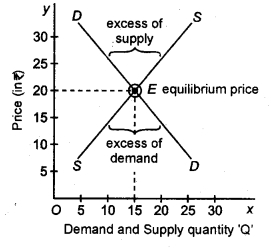

Following is the table and diagram of demand and supply of commodity ‘A’ :

It is evident from the above table and diagram that the item ‘A’ has a supply = demand = 200 units at rupees ₹ 6 per unit price, so this is the phase of equilibrium.

Question 3.

When will the equilibrium price not changed, even when the demand and supply increase?

Answer:

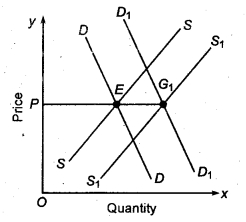

Even if there is an increase in both demand and supply, there will be no change the equilibrium price if the proportional change in demand is equal to the proportional change in supply.

Question 4.

Describe with diagram that the increase in demand and supply does not show any effect on the equilibrium price.

Answer:

In this figure, DD demand curve shifts to right to D1D1 and SS supply curve shifts to right to S1S1 and thus show equal increase, since here proportionate change has occurred in demand and supply. Thus equilibrium price keeps stable at P.

Question 5.

What will be the effect on the equilibrium price and quantity if the supply curve shifts in left and right side?

Answer:

If the supply curve shifts to the right, then the equilibrium price decreases and its quantity increases. On the contrary, if the supply curve shifts to the left, then the equilibrium price increases and its quantity decreases.

Question 6.

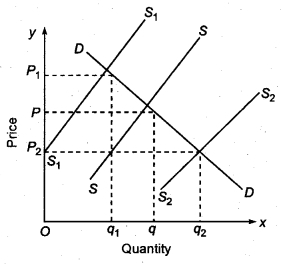

What will be the effect on the equilibrium price and quantity if the supply curve shifts to the left and right side? Explain it by a diagram.

Answer:

Due to increase in supply, supply curve shift towards the right and new supply curve is S1S1 and new equilibrium point is E1 New equilibrium price OP1 and new equilibrium quantity is OQ1 Suppose supply decreases, then the supply will shift towards left only. New supply curve is S2S2. New equilibrium point is E2. New equilibrium price is OP2 and new equilibrium quantity reduces from OQ to Q2.

It is clear that due to changes in supply, its equilibrium prices changes in the opposite direction. With increase in supply, equilibrium price decreases, and with decrease in supply, equilibrium price increases.

Question 7.

What will be the effect of shift in demand curve on the price and quantity of equilibrium?

Answer:

If the demand curve is shifted on the right side, then both equilibrium price and quantity will increase. On the contrary, if the demand curve shifts to the left side, then there is a decrease in equilibrium price and quantity.

Question 8.

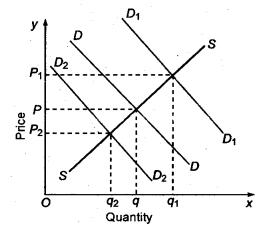

What will be the effect of shift in demand curve on the price and quantity of equilibrium? Clarify it by diagram.

Answer:

On X axis, quantity of demand and supply are given, and on Y axis, price of good X have been taken. Initial equilibrium of demand and supply is at E. Therefore, equilibrium price is OP and equilibrium quantity is OQ. Other things being equal, if demand increases; equilibrium price will increase to OP1, and with decrease in demand, equilibrium price will decrease to OP2.

Question 9.

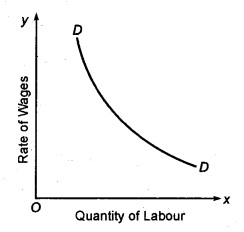

Explain with a diagram that in short term, the law of demand applies on demand of labour.

Answer:

From the diagram, it is clear that the demand for labour slopes downwards from left to right. It is an indicator of the fact that the demand for labour decreases when the wage rate is high, and the demand for labour becomes greater when the wage rate is low.

Question 10.

What do you understand by supply of labour in perfectly competitive market?

Answer:

The supply of labour refers to the hours or days of labour, not the number of workers. Labour is from homes and families where the workers live. Therefore, the workers are labour and the firms are the purchasers of labour.

Question 11.

What do you understand by maximum fixed price?

Answer:

The price fixed by the government which is less than the equilibrium price of a commodity (which is high) is called Maximum fixed price or controlled price. In this provision, the government rations things to make them available to poorer sections.

Question 12.

What do you understand by minimum fixed price?

Answer:

If the equilibrium price is low in the market, then the government determines the value of agricultural produce above the equilibrium price to protect the interests of farmers. This support price is called the minimum fixed price. The government purchases the remaining produce at this price.

Question 13.

Explain the supply of labour by a diagram, in the perfectly competitive market.

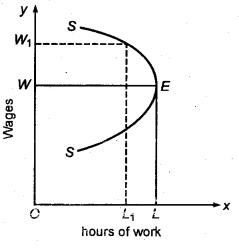

Answer:

In the figure, SS is the labour curve that is seen bending backwards after point E, since when the wages of worker was OW, he worked OL hours, but when wages become OW1, he rested more because of income affect and working hours reduced to OL1

Question 14.

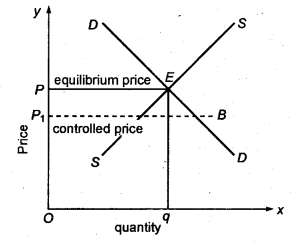

Show the price controlled by the government through a diagram.

Answer:

In the figure, SS is supply curve and DD is demand curve. P is equilibrium price, q is equilibrium quantity. Government fixes controlled price lesser than equilibrium price, and thus P1 shows controlled price. Thus, here price is reduced from OP to OP1.

Question 15.

Clarify the concept of market price.

Answer:

Market price is the value that is determined by the market forces, i.e. demand and supply. It is the price fixed in the short and very short term. It has a tendency to change quickly.

Question 16.

What do you mean by normal price?

Answer:

The normal price concept is related to the long-term market. In normal pricing, the contribution of the supply side is higher than the demand side, because in the long run, supply can be varied according to the demand for supply. Hence, it is also called long term or permanent price.

Question 17.

What is the difference between goods market and labour market? Clarify it.

Answer:

Demand for commodity market is from households, whereas labour market demand comes from producer firms, and the supply of commodity market is from producer firms, while the labour market is supplied by household families.

Question 18.

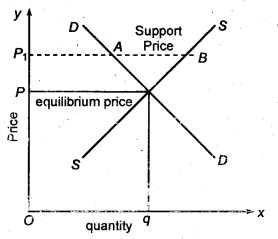

Explain the minimum support price by diagram.

Answer:

In the figure, SS is supply curve, DD is demand curve, OP is equilibiriom price, Oq the equilibrium quantity. Government fixes support price above equilibriuom price at OP1 which is the minimum fixed price for the product. Here, price is increased from OP to OP1.

Question 19.

Explain the marginal aquisition product of labour.

Answer:

The additional benefits gained from the use of each additional unit of labour are equivalent to the product of marginal acquisition and marginal product. It is called the marginal acquisition product of labour. It is displayed by W.

Question 20.

Explain marginal product price of labour.

Answer:

The marginal product price of labour is calculated by multiplying the increase in the production by the use of each additional unit of labour, with the market price. The price of the marginal product of labour for the perfectly competitive firm is equal to the marginal acquisition product of labour.

Question 21.

Explain the market equilibrium.

Answer:

Condition of market in which total market supply is equal to total market demand ‘ is called market equilibrium. In this situation, there is no motivation for any change in demand and supply. Market equilibrium is also alternately called zero excess demand zero ; excess supply.

Formulae:

Y3 = YD

Here Ys = Market supply, YD = Market demand.

Question 22.

When do we say that there is an excess demand in market?

Answer:

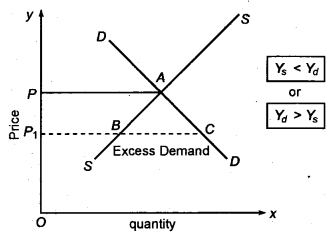

Excess demand in market refers to a situation where the quantity demanded for a good exceeds the quantity supplied of that good. It occurs when price of good is below the market price for the given demand curve and supply curve.

In the above given diagram, SS is market supply curve, DD is market demand curve, A is equilibrium point, OP is equilibrium price, OP1 is market price and excess demand is BC.

Question 23.

When do we say that there is an excess supply in market?

Answer:

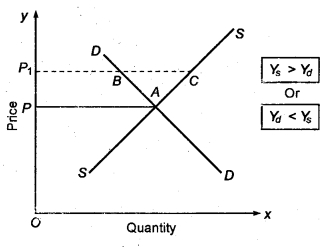

When the market price exceeds the equilibrium price, consumers demand a lower quantity of goods, thereby increasing the quantity of good than supplied. This situation is called excess supply.

Here, SS is supply curve, DD the demand curve, A equilibrium point, OP equilibrium price, OP1 market price and BC shows excess supply.

Question 24.

What happens if the prevailing price in the market is :

(a) More than the equilibrium price

(b) Less than the equilibrium price.

Answer:

(i) If the prevailing price in the market is more than the equilibrium price, then total market demand will decrease and total market supply will increase.

(ii) If the prevailing price in the market is less than the equilibrium price, then the total market demand will increase and the total market supply will decrease. Therefore, if the prevailing price in the market is lower than the price, then the excess demand situation will arise in the market.

Question 25.

Suppose that the equilibrium price is higher than the minimum average cost of firms in the market. If we allow uninterrupted entry and exit of firms, how will the market adjust with the price?

Answer:

The minimum average cost of the firm is the equilibrium price, therefore, the higher the average cost of the market price, means that the market price will exceed the equilibrium price in such a situation. But in order to earn profit, firms will enter the market faster. In this case, total supply will be equal to the total demand, and the market price will be equal to the average minimum cost or equilibrium price.

Question 26.

When the market permits uninterrupted entry and exit, then at what level of price does the perfect competition market is satisfied ? How is the equilibrium quantity determined in such a market?

Answer:

Firms supply the minimum average cost or balance at the price level. In such a market, the balance quantity is determined at the point where the price line intersects the market demand curve.

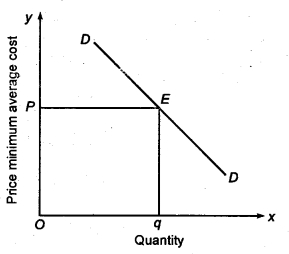

OP is the equilibrium price, DD is demand curve, E is equilibrium point and OQ equilibrium quantity. From the picture, it is clear that the price is intersecting the demand P on the demand curve DD on the E point. So, the equilibrium quantity will be OQ.

Question 27.

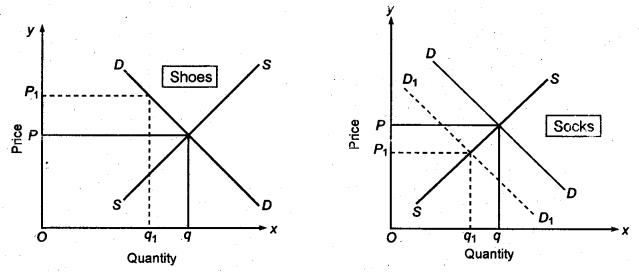

By using supply and demand curves, show how does the increase price of shoes influences the sale and purchase price and quantity of pair of socks?

Answer:

Socks and shoes are used together. So, they are complementary goods. According to the diagram on left, due to increase in price, the demand of shoes decreases, and with that, the demand of socks also decreases. So, its price also decreases.

According to the figure on right the demand of socks decreases from Q to Q1 and the price decreases from P to P1 Whereas the demand curve shifts from DD to D1D1

Question 28.

Suppose that the demand and supply of commodity x in the perfectly competitive market,- is given in the following ways-

QD = 700 – P

QS = 500 + 3P because P > 15

QS = 0 because 0 < P < 15

Suppose that the homogeneous firms are in the market. Find out the cause of the market supply being zero at the cost of less than ₹ 15. What is the equilibrium price of this commodity? In the condition of equilibrium, how much of the quantity of commodity x is produced?

Answer:

Suppose that the number of homogeneous firm is fixed, then given –

QD = 700 – P

QS = 500 + 3P here P > 15

QS = 0 here P < 15

here, QD = Demand, QS = Supply, P = Price

Because the market becomes empty at the balance price, therefore, we can determine the balance value by comparing the market demand and market supply –

QD = QS

700 – P = 500 + 3P

700 – 500 = 3P + P

4P = 200

P = 50

Thus, Equilibrium Price = ₹ 50 per unit

So, in the condition of equilibrium, commodity x’s quantity QD = 700 – 50 = 650 units Supply QS = 500 + (3 × 50) = 650 units

Similarly, the equilibrium quantity is 650 units and firms will not produce anything less than ₹ 50 because they will suffer loss.

RBSE Class 12 Economics Chapter 13 Long Answer Type Questions

Question 1.

Explain market equilibrium. Show through diagrams the effect on equilibrium quantity and price when the supply curve shifts to the right and demand curve shifts to the right.

Answer:

Market equilibrium is a situation of market in which demand for a commodity is exactly equal to its supply, corresponding to a particular price. Thus, in a state of equilibrium, the market clears itself as market demand = market supply of the commodity. There is neither excess demand nor excess supply. In such a situation, the price that prevails in the market is called equilibrium price. It is called general theory of price determination or price determination theory of demand and supply.

Marshall assumes that price of a commodity is neither determined by demand nor supply of the commodity, but it is rather determined by both – the forces of demand and supply.

According to Prof. J.K.Mehta, “Equilibrium denotes lack of change”.

According to Prof. Boulding, “A mechanical analogy may be found in a ball rolling at a constant speed or better still of a forest in equilibrium where Tree-sprout grows or dies but where the composite of the forest as a whole remains unchanged.”

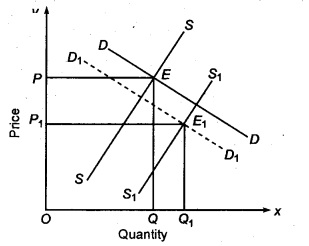

When supply curve shifts to the right qnd demand curve shifts to the left, the equilibirum price decreases, while equilibrium quantity remains unchanged. The change in equilibrium will depend on how much decrease will occur in demand and how much increase occurs in supply. We can understand this variation on the following basis :

(i) When decrease in demand is less, and increase in supply is more – Here, in the figure, when demand reduces, the new demand curve will be D1D1, and with increase in supply, new supply curve is S1S1, and equilibrium is at Ex; Thus, equilibrium price reduces from OP to OP1 whereas equilibrium quantity increases from OQ to OQ1 Where price reduces more, quantity reduces less in proportion to price.

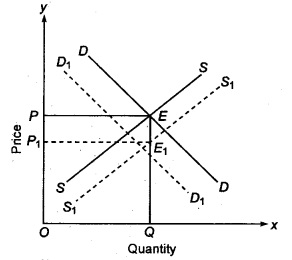

(ii) When decrease in demand and increase in supply are euqal – The diagram clarifies this, that reduction in demand makes new demand curve D1D1 and same increase in supply makes new supply curve S1S1, makes new equilibirum point E1. Here, equilibrium quantity remains unchanged, whereas equilibrium price reduces from OP to OP1.

(iii) When reduction in demand is more and increase in supply is less – When new demand curve D1D1 is obtained upon decrease in demand, and increase in supply gives as new supply curve S1S1, the new equilibrium point is E1. Equilibrium quantity reduces from OQ to OQ1. While price reduces from OP to OP1. Here price reduces comparatively more than quantity.

RBSE Class 12 Economics Chapter 13 Numerical Questions

Question 1.

Suppose that the demand and supply curve in a perfectly competitive market is as follows:

QD = 800 – P, QS = 500 + 3P, When P ≥ 15, QS = 0, when P < 15 Explain

(i) Why is the market supply of goods zero at any price less than 15 rupees?

(ii) What is the equilibrium price of goods?

(iii) What quantity of the product will be produced on equilibrium?

Answer:

(i) Because the minimum average cost of commodity is ₹ 15, firm will suffer loss if the firm sells commodity less than this value. So that on less than ₹ 15 the supply is zero.

(ii) Suppose the equilibrium price is P.

So QD = QS

800 – P = 500 + 3P

4P = 300

P = 75

Thus, the equilibrium price is ₹ 75.

(iii) We get the equilibrium price = ₹ 75

Thus, QD = 800 – P

= 800 – 75 = 725

QD = 500 + 3P = 500 + (3 × 75)

= 500 + 225 = 725

So, the equilibrium units = 725.

Question 2.

Suppose one commodity has the following demand and supply function.

QD = 100 – 20 P, Qs = – 5 + 15P

Find out the equilibrium price and quantity.

Answer:

For the equilibrium price :

QD = Qs

100 – 20P = – 5 + 15P

15P + 20P = 100 + 5

35P = 105

P = 3

Thus, Equilibrium price = ₹ 3 per unit

When we put these price in the equations of demand and supply, we will get the equilibrium quantity.

QD = 100 – (20 × 3) = 40

QS = – 5 + (15 × 3) = 40

Thus, Equilibrium Quantity = 40 units.

Question 3.

Suppose the equation of demand curve and the supply curve is given below. Solve the equation to know the price and quantity.

QD = 8,196 – 3,596P

QS = 600 + 4000P

Answer:

On the equilibrium price the quantity of demand and quantity of supply is equal-

So QD = QS

8,196 – 3,596 P = 600 + 4,000P

– 3,596 P – 4,000P = 600 – 8,196

7,596P = – 7,596

P = ₹ 1

Equilibrium, quantity (QD) = 8,196 – 3,596 = 4,600 units.

QD = 600 + 4,000P = 600 + (4,000 × 1) = 4,600 units.

Question 4.

The equation of the demand for laptop and the opposite fulfillment curve is given below –

P = 2QS

P = 42 – QD

Find out the equilibrium price.

Answer:

P = 2Qs or Qs = P/2

P = 42 – QD or QD = 42 – P

Equilibrium price QD = Qs

Thus from equation (i) and equation (ii)

P/2 = 42 – P

P = 84 – 2P

P + 2P = 84

3P = 84

P = 28

So Equilibrium Price = ₹ 28.

Question 5.

Suppose following are the equations of demand and supply

QD = 110 – 10P

Q = – 100 + 20P

Find out the equilibrium price and its quantity.

Answer:

We know that on the equilibrium price the demand quantity and supply quantity are equal.

So QD = Qs

That is 110 – 10P = – 100 + 20 p

Or -10 P – 20P = – 100 – 110 or -30 p = – 210 Or P = 210/30 = 7

Thus Equilibrium Price(P) = ₹ 7

Equilibrium Quantity (QD) = 110 – (10 × 7) = 40 Units

QS = – 100 + 20 × 7 = 100 + 140 = 40 units.

Question 6.

(i) Calculate the equilibrium price and quantity with the help of following equation :

QD = 10 – P

QS = P

(ii) If the market price is ₹ 7, then what will be the condition of the demand and supply of market?

(iii) If the market price is ₹ 3, then what will be the condition of the demand and supply of market?

Answer:

(i) We know on the equilibrium price QD = QS

So, 10 – P = P

-2P = – 10

P = 5

Equilibrium Price = 5

Equilibrium Quantity = 10 – P

Qs = 5 units

QD = 10 – 5 = 5units

(ii) Equilibrium price is ₹ 5 and Market price is ₹ 7. It is clear that market price is more than equilibrium price. In this market condition, there will be excess supply.

(iii) Equilibrium price is ₹ 5 and Market price is ₹ 3. It is clear that market price is less than equilibrium price. In this market condition, there will be excess demand.