RBSE Class 12 Accountancy Model Paper 1 are part of RBSE Class 12 Accountancy Board Model Papers. Here we have given RBSE Class 12 Accountancy Sample Paper 1.

| Board | RBSE |

| Textbook | SIERT, Rajasthan |

| Class | Class 12 |

| Subject | Accountancy |

| Paper Set | Model Paper 1 |

| Category | RBSE Model Papers |

RBSE Class 12 Accountancy Sample Paper 1

समयः 3.15 घण्टे

पूर्णांक : 80

परीक्षार्थियों के लिए सामान्य निर्देशः

- परीक्षार्थी सर्वप्रथम अपने प्रश्न पत्र पर नामांक अनिर्वायतः लिखें।

- सभी प्रश्न करने अनिवार्य हैं।

- प्रत्येक प्रश्न का उत्तर; दी गई उत्तर-पुस्तिका में ही लिखें।

- जिन प्रश्नों में आंतरिक खण्ड है, उन सभी के उत्तर एक साथ ही लिखें।

- यह प्रश्न पत्र दो खण्डों में विभक्त है- अ और ब। खण्ड ‘अ’ सभी छात्रों के लिए अनिवार्य है।

- खण्ड ‘ब’ के दो भाग हैं, प्रत्येक भाग में सात प्रश्न हैं। परीक्षार्थी को किसी एक भाग के सभी सात प्रश्नों को हल करना है।

-

खण्ड प्रश्न संख्या अंक प्रत्येक प्रश्न अ 1-8 1 9-14 2 15-21 4 22-23 6 ब 24-25 1 26-27 2 28-29 4 30 6 - प्रश्न संख्या 22 (खण्ड-अ) तथा 30 (खण्ड-ब) में आन्तरिक विकल्प हैं। इन प्रश्नों में से आपको एक ही विकल्प हल करना है।

खण्ड – अ

प्रश्न 1.

भारतीय साझेदारी अधिनियम कब लागू हुआ ? [1]

प्रश्न 2.

संयुक्त जीवन बीमा पॉलिसी का समर्पण मूल्य चिट्टे में कहाँ दिखाया जाता है ? [1]

प्रश्न 3.

संयुक्त जीवन बीमा पॉलिसी क्या है ? [1]

![]()

प्रश्न 4.

x, y एवं z 5 : 3 : 2 में लाभ बाँटते हुए साझेदार हैं। ख्याति पुस्तकों में नहीं दिखाई गई है लेकिन उसका मूल्य ₹ 1,00,000 है। x फर्म से अवकाश ग्रहण करता है एवं y व z भविष्य में लाभों को बराबर-बराबर बाँटते हैं। x का ख्याति में हिस्सा y वे z के खातों में किस अनुपात में डेबिट होगा ? [1]

प्रश्न 5.

वसूली खाते से आप क्या समझते हैं ? [1]

प्रश्न 6.

एक व्यक्ति वाली कम्पनी क्या है ? [1]

प्रश्न 7.

सारणी एफ. के अनुसार कम्पनी अग्रिम माँग पर कितना ब्याज दे सकती है ? [1]

प्रश्न 8.

संयुक्त साहस के माल की बिक्री पर कौन-सा खाता क्रेडिट होता है ? [1]

प्रश्न 9.

A व B एक फर्म में साझेदार हैं जो 3 : 2 के अनुपात में लाभ विभाजन करते हैं। वे C को लाभ में \(\frac {1}{5}\) हिस्से के लिए प्रवेश देते हैं। अपना पूरा हिस्सा B से प्राप्त करता है। नया लाभ विभाजन अनुपात ज्ञात करो। [2]

A and B are partners in a firm, sharing profits in the ratio of 3 : 2. C is admitted for \(\frac {1}{5}\)th share in profits of the firm which he acquired entirely from B. Calculate new Profit Sharing Ratio.

प्रश्न 10.

स्मरणार्थ संयुक्त साहस खाता क्या है? यह क्यों बनाया जाता है? [2]

![]()

प्रश्न 11.

विक्रय विवरण क्या ह ? इसे कौन तैयार करता है? [2]

प्रश्न 12.

100 टन कोयला ₹ 1,300 प्रति टन बीजक मूल्य तथा ₹ 800 प्रति टन लागत मूल्य पर भेजा गया। प्रेषक ने ₹ 20,000 खर्च किये। 76 टन कोयला एजेण्ट द्वारा बेचा गया जिस पर ₹ 8,000 विक्रय खर्च के प्रेषणी ने चुकाये। 5 टन कोयला कम होने की सूचना दी । एजेण्ट के पास बिना बिके स्टॉक का मूल्य ज्ञात करिये। [2]

100 ton coal sent on consignment for ₹ 1,300 per ton at invoice price and ₹ 800 per ton at cost price and consignor paid ₹ 20,000. Agent sold 76 ton coal and paid ₹ 8,000 for sales expenses. It is informed that 5 tonnes coal is found less. Calculate the value of remaining stock with agent.

प्रश्न 13.

अक्षय निधि कोष (Endowment Fund) से आप क्या समझते है? [2]

प्रश्न 14.

निम्नलिखित विवरण से संस्था के आय-व्यय खाते में खेल सामग्री के सम्बन्ध में व्यय की राशि ज्ञात कीजिए। [2]

(मा, शिक्षा बोर्ड संशोधित 2009)

Sports Material Payment made during the year

4,800 Outstanding Expenses on 1st Jan. 2016

900 Outstanding Expenses on 31st Dec. 2016

1,500 The Stock of Sports Material Opening ₹ 2,800 and Closing ₹ 1,200.

प्रश्न 15.

अ और ब 7 : 3 के अनुपात में लाभ बाँटते हुए साझेदार हैं। 1 अप्रैल, 2016 को उनकी पूँजी क्रमशः ₹ 1,00,000 और ₹ 40,000 थी । पूँजी एवं आहरण पर 10 प्रतिशत वार्षिक ब्याज लगाया जाना है । ब को ₹ 1,000 प्रति माह वेतन दिया जाता है। प्रत्येक माह की प्रथम तारीख को अने ₹ 1,000 प्रति माह एवं व ने ₹ 600 प्रति माह आहरण किया। पूँजी एवं आहरण पर ब्याज लगाने से पूर्व, परन्तु ब का वेतन घटाने के बाद वर्ष को लाभ ₹ 54,960 था। शुद्ध लाभ (ऐसा कमीशन घटाने के बाद) पर 5 प्रतिशत की दर से अ को कमीशन का प्रावधान करना है। उपर्युक्त सूचनाओं से 31 मार्च, 2017 का लाभ-हानि नियोजन खाता बनाइए। [4]

A and B are partners sharing profits in the ratio of 7:3. On 1st April, 2016, their capitals were ₹ 1,00,000, र 40,000 respectively. Interest is to be charged on capital and drawings at 10% per annum. B is to be allowed salary ₹ 1,000 per month. A and B withdrew ₹ 1,000 and ₹ 600 per month respectively on the first day of every month, The profits for the year, prior to calculation of interest on capitals and drawings, but after charging B’s salary amounted to ₹ 54,960. A provision for A’s commission at 5% on net profit (after charging such commission) is to be made. Prepare Profit & Loss Appropriation Account for the year ending 31st March 2017.

प्रश्न 16.

A, B C एक फर्म में साझेदार हैं जो 5 : 3 : 2 के अनुपात में लाभ विभाजन करते हैं। B अवकाश ग्रहण करता है । फर्म की ख्याति को मूल्यांकन ₹ 21,000 पर किया गया। ख्याति के लिए आवश्यक प्रविष्टियाँ कीजिए। [4]

A, B & C are partners in firm sharing profits in the ratio of 5 : 3 : 2. B retires and the goodwill of the firm is valued at ₹ 21,000. Pass necessary journal entries for treatment of goodwill.

![]()

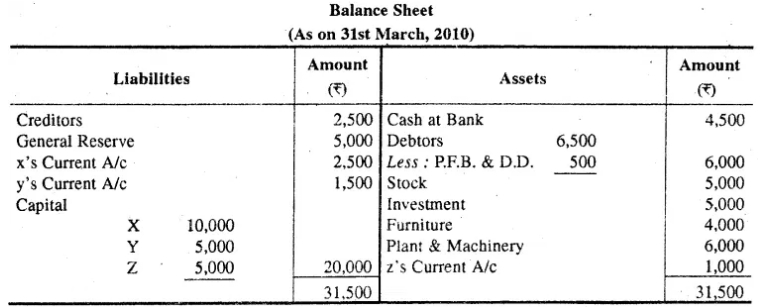

प्रश्न 17.

X, Y और Z साझेदार हैं जो लाभ-हानि को 2 : 2 : 1 अनुपात में बाँटते हैं। 31 मार्च, 2010 को साझेदारी के विघटन को सहमत हुए। उस तिथि को फर्म का चिट्ठा निम्न प्रकार था [4]

प्लाण्ट एवं मशीन से ₹ 10,000, फर्नीचर के ₹ 5,000, देनदारों से पूर्ण, स्टॉक से ₹ 4,000 प्राप्त हुए । विनियोग Z द्वारा लिये गए (पुस्तक मूल्य पर) ।लेनदारों को 10 प्रतिशत बट्टे पर भुगतान किया, वसूली व्यय ₹ 100 हुए। ₹ 550 की सम्पत्ति का पुस्तकों में लेखा नहीं किया गया था। जिसे x ने ₹ 450 में ले लिया। ₹ 100 का एक दायित्व पुस्तकों में दर्ज नहीं किया गया था। फर्म की पुस्तकों में वसूली खाता बनाइए।

प्रश्न 18.

कम्पनी के चिट्टे में निम्नलिखित मदों को आप किन शीर्षकों के अन्तर्गत रखेंगे [4]

(Under what headings will you show the following items in the Balance Sheet of the Company)

- Goodwill

- Unclaimed Dividends

- Provision for Tax

- Securities Premium

- Loose Tools

प्रश्न 19.

पवन एवं प्रत्युष एक संयुक्त साहस में भाग लेते हैं। लाभ-हानि बराबर बाँटते हुए संयुक्त साहस में प्रवेश किया। पवन ने ₹ 3,00,000 की लागत का माल संयुक्त साहस के लिये प्रेषित किया एवं उसका भाड़ा के ₹ 10,000 व अन्य व्यय के ₹ 4,000 हुए । प्रत्युष द्वारा भेजे गये माल की लागत ₹ 2,40,000 थी । उसके प्रेषण सम्बन्धी खर्चे ₹ 15,000, गोदाम किराया ₹ 5,000 हुए। माल का विक्रय पवन द्वारा किया जाना है जिस पर 2 प्रतिशत कमीशन (विक्रय मूल्य पर) देय है। पवन ने समस्त माल ₹ 6,84,000 में बेच दिया। स्मरणार्थ संयुक्त साहस खाता तथा पवन की पुस्तकों में प्रत्युष के साथ संयुक्त साहस खाता बनाइये। [4]

Pavan and Pratush entered in joint venture with sharing profit and losses equally. Pavan sent goods worth ₹ 3,00,000 and paid carriage & freight ₹ 10,000 and other expenses ₹ 4,000. Pratush sent goods worth ₹ 2,40,000 and paid consignment expenses and sundry expenses ₹ 15,000 and godown rent ₹ 5,000. Goods to be sold by Pavan. They decided 2% commission on sales. Pavan sold all the goods for ₹ 56,84,000. Prepare Memorandum joint Venture Account and Joint Venture with Pratush Account in the books of Pavan, Final payment is made through bank draft.

![]()

प्रश्न 20.

अलवर के भरत ने उदयपुर के कपिल को ₹ 1,00,000 का माल प्रेषण पर भेजा तथा ₹ 20,000 विविध व्यय के चुकाये। कपिल ने भरत को ₹ 60,000 अग्रिम भेजे। कपिल ने मजदूरी व ठेला भाड़ा के ₹ 4,000 तथा गोदाम किराये के ₹ 3,000 चुकाये। कपिल ने सम्पूर्ण माल ₹ 1,60,000 में नकद बेच दिया। प्रेषणी को विक्रय पर 5 प्रतिशत कमीशन देय है। कपिल ने शेष राशि भरत को भेज दी। आवश्यक खाते बनाइये। [4]

Mr. Bharat of Alwar sent goods to Kapil of Udaipur for ₹ 1,00,000 on consignment and paid sundry expenses T 20,000. Kapil sent ₹ 60,000 to Bharat in advance. Kapil paid wages and cartage ₹ 4,000 and godown rent ₹ 3,000. Kapil sold all the goods for ₹ 1,60,000 in cash. 5% commission on sales is payable to consignee. Kapil sent remaining amount to Bharat. Prepare necessary ledger accounts in the books of Bharat.

प्रश्न 21.

निम्नांकित सूचनाओं से प्राप्ति एवं भुगतान खाता 31 मार्च, 2017 को समाप्त होने वाले वर्ष का बनाइये। [4]

Prepare Receipts, and Payments Account for the year ending 31st March 2017 from the following information.

| प्रारम्भिक रोकड़ शेष (Cash in hand opening) | 10,000 |

| दान प्राप्त किया (Donation received) | 50,000 |

| चन्दा प्राप्त किया (Subscription received) | 1,00,000 |

| बिजली बिलों का भुगतान किया (Paid for electricity bill) | 20,000 |

| किराया र 1,000 मासिक वर्ष के दौरान 11 माह का भुगतान किया (Rent F1,000 p.m., Actually paid for 11 months during the year) | |

| कम्प्यूटर नकद में क्रय किया (Purchases of computer in cash) | 50,000 |

| मानदेय भुगतान (Honorarium paid) | 19,000 |

प्रश्न 22.

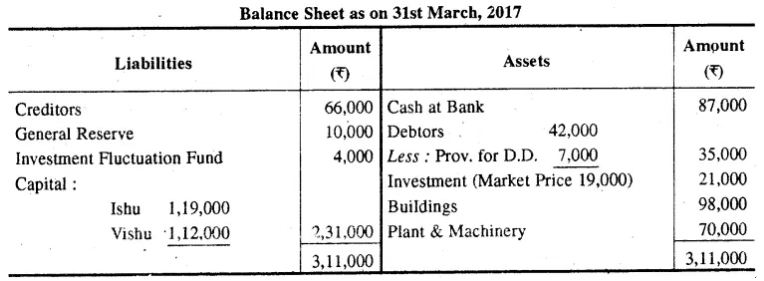

इशु और विशु 3 : 2 के अनुपात में लाभ बॉटते हुए साझेदार हैं। 31 मार्च 2017 को उनका चिट्ठा निम्न प्रकार था- [6]

Ishu and Vishu are partners sharing profits in the ratio of 3 : 2. Their Balance Sheet as on 31st March, 2017 was as follows:

नीशू को इस दिन 1/6 भाग पर निम शर्तों पर सम्मिलित किया

- नीशू ₹ 56,000 अपने हिस्से की पूँजी लाएगा।

- फर्म की ख्याति ₹ 84,000 ऑकी गई और नीशू अपना ख्याति का हिस्सा नकद लाएगा।

- प्लांट व मशीन को 20% बढ़ा दिया जाए।

- देनदार सभी उत्तम हैं।

- ₹ 9,800 का दायित्व जो लेनदारों में शामिल है, उसे नहीं देना पड़ेगा।

- नीशू की पूँजी के आधार पर इशु और विशु की पूँजी का समायोजन करें तथा कमी या अधिकता को नकद से पूरा करें । पुनर्मूल्यांकन खाता, साझेदारी के पूँजी खाते व फर्म का समायोजन के बाद स्थिति विवरण बनायें

Nishu was admitted on that date for 1/6th share on the following terms :

- Nishu will bring ₹ 56,000 as his share of capital.

- Goodwill of the firm is valued at ₹ 84,000 and Nishu will bring his share of goodwill in cash.

- Plant and Machinery be appreciated by 20%.

- all debtors are good.

- There is a liability of ₹9,800 included in Sundry creditors that is not likely to arise.

- Capital of Ishu and Vishu will be adjusted on the basis of Nishu’s capital and any excess or deficiency will be made by withdrawing or bringing in cash by concerned partner. Prepare Revaluation Account, Partner’s Capital Accounts and the Balance Sheet of the firm after the above adjustments.

![]()

अथवा

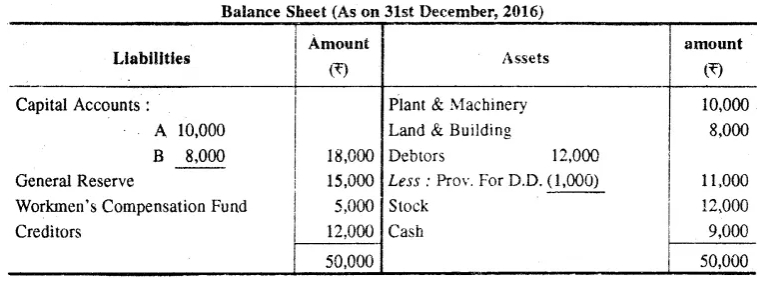

A तथा B साझेदार हैं। लाभ को 3 : 2 के अनुपात में बाँटते हैं। 31 दिसम्बर, 2016 को उनका स्थिति विवरण इस प्रकार था

A and B who are partners in a firm sharing profits in the ratio of 3 : 2. On 31st December, 2016 their Balance Sheet was as follows:

उन्होंने C को लाभ में 1/5 हिस्से के लिए निम्नलिखित शर्तों पर साझेदारी में सम्मिलित करने का निर्णय लिया–

- संदिग्ध ऋण के लिए प्रावधान को ₹ 2,000 से बढ़ा दिया जाए।

- स्टॉक के मूल्य को ₹ 4,000 से बढ़ा दिया जाए और भूमि तथा भवन के मूल्य को ₹ 18,000 तक बढ़ा दिया जाए।

- कर्मचारी क्षतिपूर्ति कोष से दायित्व ₹ 2,000 निर्धारित किया गया है।

- C ख्याति का अपना हिस्सा ₹ 10,000 नकद लाया।

- उपरोक्त पुनर्मूल्यांकन तथा समायोजन कर लेने के बाद C अपनी पूँजी के लिए A व B की संयुक्त पूँजी के 20% के बराबर राशि लाएगा पुनर्मूल्यांकन खाता, साझेदारों के पूँजी खाते और C के प्रवेश के बाद फर्म का स्थिति विवरण बनाइए।

They agreed to admit C into partnership for 1/5th share of profits on the following terms :

- Provision for doubtful debts be increased by ₹ 2,000.

- The value of stock be increased by ₹ 4,000 and Land & Building be increased to ₹ 18,000.

- The liability against workmen’s compensation fund is determined at ₹2,000.

- C brought in as his share of goodwill ₹ 10,000 in cash.

- C would bring cash as would make his capital equal to 20% of combined capital of A & B, after the above revaluation and adjustments are carried out. Prepare Revaluation Account, Partners Capital Accounts and the Balance Sheet of the firm after C’s admission.

प्रश्न 23.

मॉडर्न लि. ने ₹ 10 वाले 10,000 समता अंशों को ₹ 11 प्रति अंश की दर पर जनता में प्रस्तावित किया। राशि इस प्रकार देय थी-आवेदन पर रे 3, आबंटन पर ₹ 4 (प्रीमियम सहित) तथा प्रथम एवं अन्तिम माँग पर ₹ 4, 12,000 अंशों के लिए आवेदन प्राप्त हुए तथा संचालकों ने आनुपातिक बंटन किया। राकेश जिसने 240 अंशों के लिए आवेदन किया था, ने बंटन राशि के साथ ही माँग राशि का भुगतान कर दिया। सुकेश जिसे 100 अंश बंटित किये थे, ने बंटन राशि का भुगतान माँग राशि के साथ किया। आवश्यक जर्नल प्रविष्टियाँ दीजिए। [6]

Modern Ltd. offered to public 10,000 equity shares of ₹ 10 each at ₹ 11 per share. Amount was payable as follows on Application ₹ 3; on Allotment ₹ 4 (including premium) and on first and final call ₹ 4. Applications were received for 12,000 shares and directors allotted on pro rata basis. Rakesh, who applied for 240 shares paid call money alongwith allotment money. Sukesh to whom 100 shares were allotted paid allotment money alongwith call money. Give necessary journal entries.

खण्ड (ब)

प्रश्न 24.

क्त्तिीय विवरणों के कोई दो बाह्य उपयोगकर्ताओं के नाम लिखिए। [1]

प्रश्न 25.

सम्बन्थ के आधार पर चालू अनुपात व तरल अनुपात में अन्तर कीजिए। [1]

प्रश्न 26.

गैर-चालू दायित्व को उदाहरण सहित समझाइये। [2]

प्रश्न 27.

एक कं. की चालू सम्पत्ति ₹ 1,26,000 तथा चालू अनुपात 3 : 2 तथा स्टॉक ₹ 2,000 है। तरलता अनुपात ज्ञात कीजिए। 2 (The Current Assets of a company are ₹ 1,26,000 and the current ratio is 3 : 2 and the inventories are ₹ 2,000. Find out the liquid ratio.) [4]

प्रश्न 28.

निम्नलिखित चिट्ठे से A लिमिटेड का तुलनात्मक चिट्ठा तैयार करो [4]

(From the following Balance sheet of A Ltd. prepare comparative balance sheet)

प्रश्न 29.

पेशेवर लेखाकार का नैतिकता से क्या सरोकार है ? [4]

प्रश्न 30.

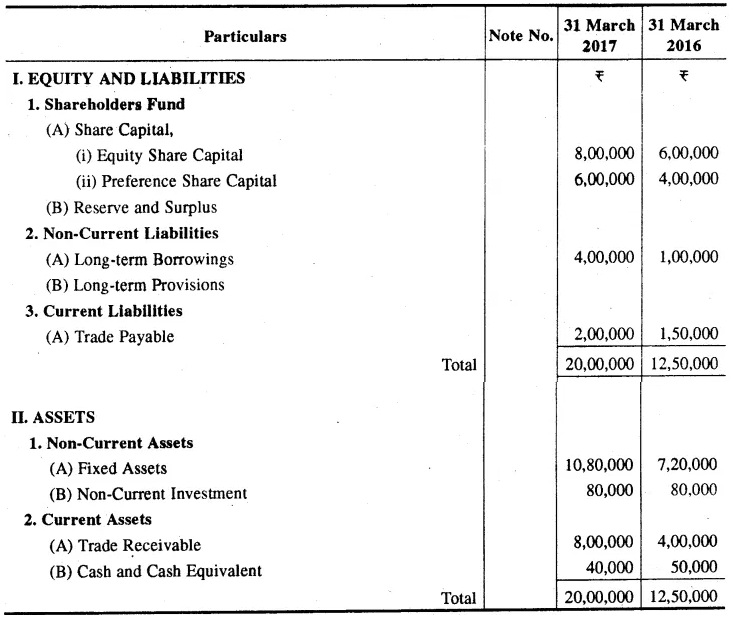

तन्वी लि. की निम्नलिखित सूचनाओं से गणना कीजिए(From the following informations of Tanvi Ltd. Calculate [6]

- कार्यशील पूँजी अनुपात (Working Capital Ratio),

- त्वरित अनुपात (Quick Ratio);

- स्कन्ध आवर्त अनुपात (Inventory Turnover Ratio);

- सकल लाभ अनुपात (Gross Profit Ratio);

- शोधन, क्षमता अनुपात (Solvency Ratio),

- परिचालन अनुपात (Operating Ratio),

- परिचालन लाभ अनुपात (Operating Profit Ratio),

- शुद्ध लाभ अनुपात (Net Profit Ratio)

सूचनाएँ (Informations)—परिचालन से आय (Revenue from operations) ₹ 2,00,000; क्रय (Purchases) ₹ 1,20,000; प्रारम्भिक स्कन्ध (Opening Inventory) ₹ 12,000; अन्तिम स्कन्ध (Closing Inventory) ₹ 18,000; मजदूरी (Wages) ₹ 8,000; विक्रय व्यय (Selling Expenses) के ₹ 2,000; मूर्त स्थायी सम्पत्तियाँ (Tangible Fixed Assets). ₹ 2,12,000; अन्य चालू सम्पत्तियाँ (Other Current Assets) ₹ 50,000; चालू दायित्व (Current Liabilities) ₹ 30,000; संमती अंश पूँजी (Equity Share Capital) ₹ 1,00,000; 7% पूर्वाधिकार अंश पूँजी (7% Preference Share Capital) ₹ 80,000; संचय (Reserves) ₹ 10,000; तथा 8% ऋणपत्र (8% Debentures) ₹ 60,000.

![]()

अथवा

ऋषभ लि. की निम्नलिखित सूचनाओं से ज्ञात कीजिए(From the following informations of Rishabh Ltd. find out :

- सकल लाभ अनुपात (Gross Profit Ratio)

- परिचालन अनुपाते (Operating Ratio)

- परिचालन लाभ अनुपात (Operating Profit Ratio)

- शुद्ध लाभ अनुपात (Net Profit Ratio)

- विनियोग पर प्रत्याय (Return on Investment)

- ब्याज व्याप्ति अनुपात (Interest Coverage Ratio)

सूचनाएँ (Informations)—संचालन क्रियाओं से आगम (Revenue from operations) ₹ 4,00,000, संचालन क्रियाओं से आगम की लागत (Cost of Revenue from operations) ₹ 2,25,000, अल्पकालीन ऋणों पर ब्याज (Interest on Short-term Loan) ₹ 5,000, कार्यालय व्यय (Office Expenses) ₹ 25,000, विक्रय व्यय (Selling Expenses) ₹ 50,000, प्राप्त किराया (Rent Received) ₹ 4,000, अग्नि से हानि (Loss by Fire) ₹ 10,000, दीर्घकालीन ऋणों पर ब्याज (Interest on Long-term Loan) ₹ 10,000, कमीशन प्राप्त (Commission Received) ₹ 5,000, विनियोजित पूँजी (Capital Employed) ₹ 6,00,000, आयकर की दर 30% (Income Tax rate 30%)

उत्तरम्

उत्तर 1:

1 अक्टूबर 1932 को।

उत्तर 2:

संयुक्त जीवन बीमा पॉलिसी का समर्पण मूल्य चिट्टे के सम्पत्ति पक्ष में दिखाया जाता है।

उत्तर 3:

फर्म द्वारा सभी साझेदारों के जीवन पर संयुक्त रूप से ली गई जीवन बीमा पॉलिसी ही संयुक्त जीवन बीमा पॉलिसी कहलाती है।

उत्तर 4:

x का ख्याति में हिस्सा y व 2 के खातों में 2 : 3 के अनुपात में डेबिट होगा।

उत्तर 5:

फर्म के समापन पर फर्म की सम्पत्तियों का विक्रय करके राशि वसूल की जाती है तथा फर्म के दायित्वों का भुगतान किया जाता है। इस कार्य के लिए फर्म की पुस्तकों में एक विशेष प्रकार का खाता खोला जाता है। जिसे वसूली खाता कहते हैं।

उत्तर 6:

एक व्यक्ति वाली कम्पनी से आशय उस कम्पनी से है जिसमें एक ही व्यक्ति सदस्य के रूप में होता है।

उत्तर 7:

12 प्रतिशत।

![]()

उत्तर 8:

संयुक्त साहस खाता।

उत्तर 9:

C को लाभ में हिस्सा = \(\frac {1}{5}\), A का लाभ में हिस्सा = \(\frac {3}{5}\)

B का नया लभ = \(\frac {2}{5} – \frac {1}{5} = \frac {1}{5}\)

नया लाभ विभाजन अनुपात = \(\frac {1}{5}:\frac {1}{5}:\frac {1}{5} = 3 : 1 : 1\)

उत्तर 10:

जब केवल स्वयं के लेन-देनों का लेखा संयुक्त साहसी द्वारा किया जाता है तो संयुक्त साहस कार्य समाप्त होने पर एक दूसरे साहसी को अपने लेन-देनों की नकल भेज दी जाती है। तब प्रत्येक साहसी अपनी पुस्तकों में एक खाता बनाता है जिसे स्मरणार्थ संयुक्त साहस खाता कहते हैं।

समस्त साहसियों द्वारा किये गये व्यवहारों को लेखा करने के उपरान्त ही संयुक्त साहस के लाभ-हानि का पता लगाने के लिए व शुद्ध देय/लेय राशि की जानकारी के लिए स्मरणार्थ संयुक्त साहस खाता बनाया जाता है।

उत्तर 11:

प्रेषणी द्वारा माल के विक्रय के पश्चात् प्रेषक को भेजा गया विवरण विक्रय विवरण कहलाता है जिसमें बेचे गये माल की किस्म, मात्रा, विक्रय मूल्य, कमीशन, प्रेषण पर अग्रिम आदि का विवरण होता है। इसे एजेण्ट द्वारा तैयार किया जाता है।

उत्तर 12:

उत्तर 13:

सम्पत्ति से प्राप्त ऐसी राशि जिसकी आय का उपयोग दान दाता द्वारा बताए गए विशेष उद्देश्य के लिए किया जायेगी तथा मूल सम्पत्ति सदा यथा स्थिति में रहेगी अर्थात् उसका उपयोग नहीं किया जायेगा, उसे अक्षय निधि कोण कहते हैं।

![]()

उत्तर 14:

Sports Material Consume

| Opening Stock of Sports Material | ₹ 2,800 |

| Payment made during the year Creditors | — |

| for sports material as on Dec. 16 | ₹ 6,300 |

| ₹ 9,100 |

| Less : Closing Stock of Sports Material | ₹ 1,200 | |

| Creditors for Sports material Jan. 16 | ₹ 900 | ₹ 2,100 |

| Sports Material Consumed Shown In Income & Expenditure A/c | ₹ 7,000 |

उत्तर 15:

Dr.

Profit & Loss Appropriation A/c (31 March, 2017)

Working Note :

1. Calculation of Interest on Drawings

A’s Drawings = ₹ 1,000 x 12 = ₹ 12,000

Interest on Drawings of A = \(\frac {12,000\times 6.5\times 10}{100\times 12}\) = ₹ 650

B’s Drawings = 600 × 12 = ₹ 77,200

Interest on Drawings of B = \(\frac {7,200\times 6.5\times 10}{100\times 12}\) = ₹ 390

2. Calculation of A’s Commission = 68,000 – 26,000 = ₹ 42,000

\(=\frac {42,000\times 5}{150}\) = ₹ 2,000

उत्तर 16:

प्राप्ति अनुपात (Gain Ratio) = नया अनुपात – पुराना अनुपात

A का फायदा = \(\frac {5}{7} – \frac {5}{10} = \frac {50 – 35}{70} = \frac {15}{70}\)

C का फायदा = \(\frac {2}{7} – \frac {2}{10} = \frac {20 – 14}{70} = \frac {6}{70}\)

A तथा C का फायदे का अनुपात = \(\frac {15}{70}:\frac {6}{70} = 15 : 6 = 5 : 2\)

| A’s Capital Alc Dr. | 4,500 | |

| C’s Capital A/C Dr. | 1,800 | |

| To B’s Capital Alc (Being retiring partner’s share of goodwill adjusted to remaining partner’s in their gaining ratio.) |

6,300 |

![]()

उत्तर 17:

Realisation Account

उत्तर 18:

| Items | Headings |

| 1. Goodwill | Intangible Assets under ‘Fixed Assets’ |

| 2. Unclaimed Dividends | Current Liabilities |

| 3. Provision for Tax | Short-term provisions under Current Liabilities |

| 4. Securities Premium | Reserves and Surplus, under Shareholders Fund |

| 5. Loose Tools | Inventories under ‘Current Assets’ |

उत्तर 19:

उत्तर 20:

उत्तर 21:

उत्तर 22:

![]()

उत्तर 23:

खण्ड (ब)

उत्तर 24:

- बैंक व वित्तीय संस्थाएँ

- लेनदार।

उत्तर 25:

चालू अनुपात चालू सम्पत्तियों व चालू दायित्वों के मध्य सम्बन्ध दर्शाता है जबकि तरल अनुपात तरलसम्पत्तियों एवं चालू दायित्वों के मध्य सम्बन्ध दर्शाता है।

उत्तर 26:

कम्पनी अधिनियम 2013 की अनुसूची III के अनुसार, वे दायित्व जो चालू दायित्वों की श्रेणी में नहीं आते हैं उन्हें गैर-चालू दायित्व कहते हैं, जैसे—दीर्घकालीन ऋण, स्थगित कर दायित्व, दीर्घकालीन आयोजन तथा अन्य दीर्घकालीन दायित्वों को इस श्रेणी में शामिल किया जाता है।

उत्तर 27:

![]()

उत्तर 28:

उत्तर 29:

पेशेवर लेखाकार की समाज में महत्वपूर्ण भूमिका होती है। विनियोगकर्ता, कर्मचारी,ऋणदाता, सरकार तथा जनसामान्य पेशेवर लेखाकारों पर निर्भर रहते हैं। पेशेवर लेखाकार की सबसे मूल्यवान सम्पत्ति उसकी ईमानदार छवि होती है। इनके कार्यों प्रभावशाली वित्तीय प्रबन्ध तथा व्यवसाय व कर से सम्बन्धित मामलों में प्रभावपूर्ण सलाह आदि प्रमुख हैं। पेशेवर लेखकारों का ऐसी सेवाओं को प्रदान करने में आचरण एवं व्यवहार देश की आर्थिक खुशहाली पर प्रभाव डालता है।

अतः पेशेवर लेखाकारों से यह आशा की जाती है कि वे समाज को अपनी सर्वश्रेष्ठ सेवाएँ देंगे जो नैतिक आवश्यकताओं के अनुकूल होंगी। पेशेवर लेखाकारों के विभिन्न संस्थानों, जैसे—भारतीय चार्टर्ड अकाउन्टेन्ट संस्थान आदि ने अपने सदस्यों के लिए आचार संहितायें लागू कर रखी हैं जिससे पेशेवर लेखाकारों का उच्च नैतिक व्यवहार सुनिश्चित किया जा सके।

उत्तर 30:

>

>

We hope the given RBSE Class 12 Accountancy Model Paper 1 will help you. If you have any query regarding RBSE Class 12 Accountancy Sample Paper 1, drop a comment below and we will get back to you at the earliest.